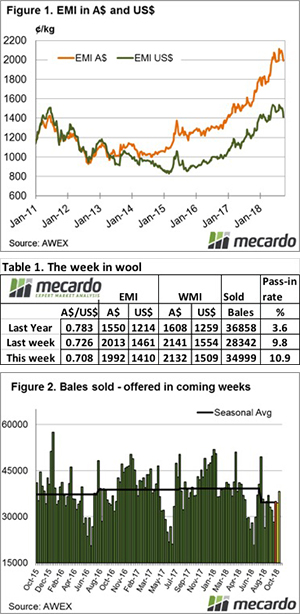

It seems that Fremantle was the “canary in the mine” last week. We reported that the market appeared to find support in WA late on Thursday and this translated into a stronger market this week.

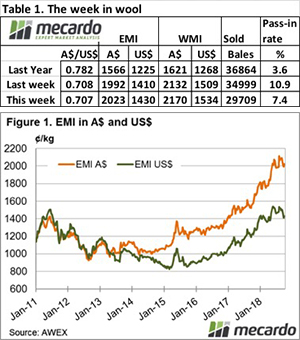

The Eastern Market Indicator (EMI) picked up 31 cents for the week, settling back above 2,000 cents again, to end the week at 2,023 cents in Au$. The EMI in US$ terms was not quite a strong with the market receiving some benefit from Au$ movements, posting a 20 cents improvement to finish at 1,430 US cents (Table 1).

Last Thursday, Fremantle provided the confidence into this week. It also continued this trend to see the WMI gain a further 38 cents to end the week at 2,170 cents.

With a resurgent market, the Pass-in rate dropped below double-digit figures, with 7.4% of the total offering passed. This resulted in a clearance to the trade for the week of 29,709 bales, with 2,363 bales passed. There was a reduced dollar value for the week of $68.74 million and a combined value of $982.58 million so far this season.

In the nine auction weeks since the winter recess, 341,922 bales have been cleared to the trade, 46,600 fewer than the same period last year. The average shortfall cleared to the trade compared to the same time last year now sits at 4,660 bales per week (Figure 2).

Strongest demand this week came for 18.5 and broader types, with 21 & 22 MPG in Melbourne lifting almost 100 cents. There was a large offering of fine tender wool which struggled to attract sufficient demand and weighed down the fine wool market.

As noted in the Mecardo article, Fine wool volumes rising, the drought will increase this sector of the market and at the same time reduce the volume of broader types. We are seeing this play out in the market now, impacting & driving price movements.

An increase in fine Merino volumes has been anticipated due to the dry conditions in eastern sheep regions. This is starting to happen in earnest now, as the production from the higher rainfall regions in eastern Australia (which is finer to begin with), shows the effect of drought. This trend in supply will persist through to at least mid-2019, therefore the downward trend on fine wool premiums will persist for the same time.

Crossbreds prices remained firm, but it was noted that the better-prepared wools performed well while poorly prepared clips struggled with a much higher pass-in rate.

Cardings produced a mixed bag, cheaper in Melbourne, dearer in Fremantle and no change in Sydney.

The week ahead

Next week a slightly larger offering of 37,644 bales is rostered, and with Fremantle again providing a solid finish to the market we should see some level of support for the market.

The next 3 weeks have rostered 37k bales, and while the spring shearing is causing a slight increase week on week, it will be down around 20k on the same period last year.

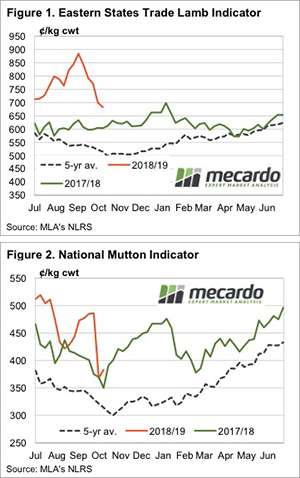

The market was moving along predictably enough. On Wednesday the Eastern States Trade Lamb Indicator (ESTLI) was down 57¢, hitting a 3 month low to 676¢/kg cwt.

The market was moving along predictably enough. On Wednesday the Eastern States Trade Lamb Indicator (ESTLI) was down 57¢, hitting a 3 month low to 676¢/kg cwt.

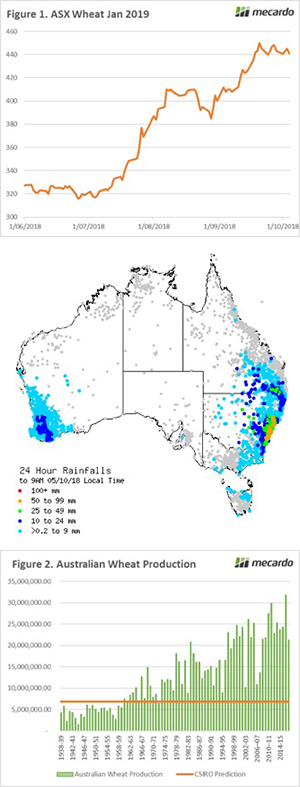

The drought continues to be the main talking point, with this September being officially the driest on record. The areas that were in reasonable condition at the start of the month (Vic, SA & WA) have all seen downgrades to their potential production. However, it’s not all doom and gloom with welcome rainfall in NSW.

The drought continues to be the main talking point, with this September being officially the driest on record. The areas that were in reasonable condition at the start of the month (Vic, SA & WA) have all seen downgrades to their potential production. However, it’s not all doom and gloom with welcome rainfall in NSW.