Pre-Easter supply glut fails to dampen price

Prices for all NLRS reported categories of east coast lamb and sheep have risen from levels recorded in mid-March, despite most measures of supply reaching toward seasonal highs. Most categories of lamb are fetching over 700¢ and mutton is holding above 500¢ this week.

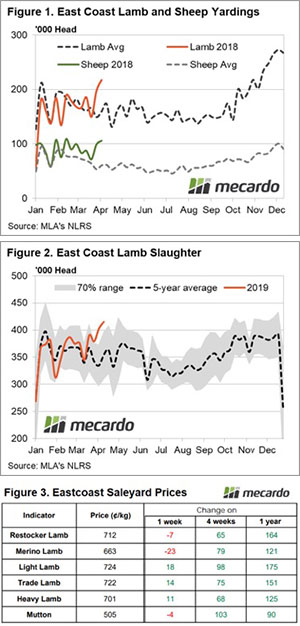

Since mid-March lamb throughput across the east coast has been running 18% higher than the pattern set by the five-year trend and sheep yarding levels have been more pronounced, averaging weekly levels 47% above the five-year trend (Figure 1).

A similar picture has emerged for East coast lamb slaughter with average weekly levels running nearly 14% higher than the five-year average trend (Figure 2). The higher supply is having limited impact upon prices as meat works seem to be happy soaking up the additional supply prior to the Easter period slowdown.

A summary of saleyard price movements highlights the market strength over the past four weeks in the face of the higher supply. All categories registering closing prices this week that are around 70¢ to 100¢ higher than a month ago (Figure 3).

The Eastern States Trade Lamb Indicator (ESTLI) managed a 2% gain on the week to close at 722¢/kg cwt. In the West, trade lambs managed to climb also, up nearly 1% on the mid-week price summary from Meat and Livestock Australia, but were unable to break above the 700¢ level yet at 679¢/kg cwt.

What does it mean/next week?:

Reduced sales and a lighter offering is expected as we hit the Easter lull so it’s unlikely to see prices retreat too much in the coming weeks. Although the forecast for rain into the next week is pretty light on and without a clear sign of a decent Autumn break in the south there will be limited opportunities for prices to surge too much higher.