Fact or fiction?

Sometimes the hardest thing to do when looking at markets is to decipher the real message from the published message. There is a lot of rhetoric around the China imports and US exports of grain and beans, with polarized stories representing positive and negative positions. It seems that “fake” news is a distinct possibility.

Usually this misinformation revolves around supply, but its intention is to influence market prices. The best approach in understanding the real picture is to refer to the data.

The University of Illinois in their Farm Policy News (FPN), reported that last week was the largest sale of soybeans so far this marketing year was enacted. While 39% of this was to China, a further 39% was to “unknown”, with FPN speculating that this “very likely a lot/most to China” also

When combining other “facts”, the answer becomes even more obvious. Under the agreed trade deal between China & the US, China agreed to take $36.5 billion in American agricultural goods in 2020. In the first 4 months with the disruption as a result of COVID-19, only $4.65 billion was exported.

Both sides have said they have a commitment to honoring the phase 1 deal, so expect a ramping up of activity in the next couple of quarters.

In related news, FPN reported “The American Farm Bureau Federation on Wednesday sent a detailed list of recommendations to Congress to help farmers, stating that even though lawmakers had provided earlier aid, more is needed because of economic losses facing the industry.”

This aid is running into the billions, and with corn prices falling 50 cents per pound to around US$3.20, the National Corn Growers Association calculates a loss of $49 per acre, they are asking for more.

Subsidies are in the news at the moment, (see China barley tariff report) but the consequence of this US government support will be to incentivize US growers to plant, causing the supply demand message to be muted and the continuous high level of world stocks to remain.

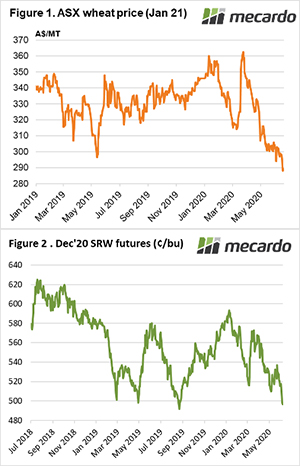

The ASX Jan 2021 contract slowly eased this week to end 10 dollars lower at $288, while the US CME Dec 2020 contract pulled back further, ending the week just under $497.

Domestic delivered prices tended to firm this week as buyers sought supply while growers were cautious in accepting old crop pricing, with it still a month or two away before producers have the confidence to sell “new crop”.

Next week?

Weather is all important in influencing grain prices, especially at this time of the year the weather in the Northern hemisphere. This week the news from the US is that after a period of dry the forecast is for rainfall over the next 7 days is predicted, this had the expected result of causing the market to soften.