ABARES forecasting more lambs but demand to drive.

The Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) are good enough to have a crack at forecasting financial year lamb slaughter. This week we take a look into this, assume their December forecasts are right, and see what it means for second half lamb supply.

Regular readers will know that forecasting supply of any agricultural commodity is an imprecise art. With livestock, in particular sheep, it’s even harder. The starting number of sheep is always rubbery. Good seasons can see tightening supply and poor seasons heavy increases. Add to this variation in lambing percentages and on the same starting flock we have in the past seen variation of 10-15% in lamb supply.

an imprecise art. With livestock, in particular sheep, it’s even harder. The starting number of sheep is always rubbery. Good seasons can see tightening supply and poor seasons heavy increases. Add to this variation in lambing percentages and on the same starting flock we have in the past seen variation of 10-15% in lamb supply.

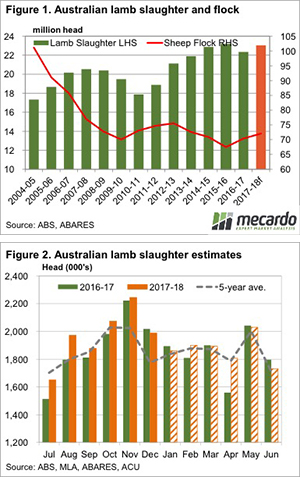

Regardless of all this, ABARES have come out with what seems to be a reasonable number for 2017-18 lamb slaughter, pegging it at 23.03 million head (figure 1). The slaughter forecast is 3% higher than slaughter for 2016-17, and the five year average. The higher slaughter numbers are a result of growth in the flock, driven by lower lamb turnoff last year.

ABARES are forecasting the national sheep flock to finish 2017-18 at 72.6 million head. This is also 3% higher than June 2017, and will take the flock to a four year high, which, we would think, will drive lamb slaughter in coming years.

In the more immediate term, we can make some rough estimates of how lamb slaughter might play out for the next six months based on the ABARES forecast, and what has been slaughtered to date.

Figure 2 shows lamb slaughter for the year to date, based on Australian Bureau of Statistics (ABS) figures to October, and our estimates for November and December, based on MLA’s weekly numbers. Slaughter for the year to date has run around 3% higher than last year. This means that some of the forecast higher supply has already exited the market.

For the second half of the year we have deducted slaughter to date from ABARES forecast 23.03 million head. This leaves 11.22 million head, to which we have applied average seasonality to come up with monthly slaughter estimates.

Key points:

- ABARES December Agricultural Commodities Report pegged 17-18 lamb slaughter 3% higher than last year.

- To date lamb slaughter has been running 3% higher than last year, with remaining lambs to lift second half slaughter rates.

- Strong demand for lamb has driven record spring prices so far, but strong supply will temper further rises.

What does this mean?

There are a couple of things to take from this analysis. Firstly, lambs slaughter for the coming six months is likely to be higher than last year. This should temper price rises to an extent. If demand was at the same level as last year, we’d expect lamb prices to be lower than last year.

However, the second thing we can see in figure 2 is that lamb supply is also likely to be much weaker than it was from October to December. We have been banging on about stronger demand driving prices higher during spring. If demand remains strong, prices are likely to better than last year even with stronger supply.