Canola – Seeding vs harvest

After having spoken with farmers across Australia and with agronomy companies it is all but certain that canola acreage will be dramatically increased for the 2017/18 season. In this analysis, we look back to the past to see whether historically having cover at seeding has been beneficial.

All going well, and with the rain landing in the right places at the right time, Australia can be expected to have a bumper canola crop. This is a story likely to be repeated across the rest of the world with the fall in cereal prices.

All going well, and with the rain landing in the right places at the right time, Australia can be expected to have a bumper canola crop. This is a story likely to be repeated across the rest of the world with the fall in cereal prices.

As is the case with wheat pricing, the local canola price is derived from a futures price. The futures used for pricing canola are either the ICE canola (Winnipeg) and Matif rapeseed (Paris) contracts.

In our discussions with growers and buyers the question often asked in recent weeks has been “How often are canola prices lower at harvest compared to seeding?”. It’s an important question to ask, as looking back at historical data can assist with decision making.

In this analysis, we have excluded basis and currency to focus on the futures component of our pricing, as this makes up the lion’s share of any movement. The methodology was to average the price of the November contract in April from 1995 to 2016, and look for the percentage change for each season between April and the average harvest spot futures.

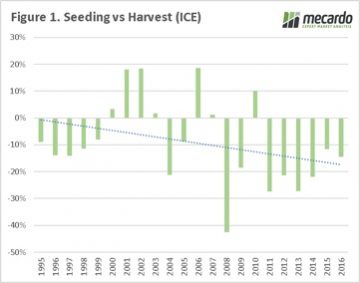

In figure 1 the ICE contract is used, and it is quite glaring that in the 22 years charted, that only in 7 years has the contract been higher at harvest than at seeding. The average change from seeding to harvest is minus 9%.

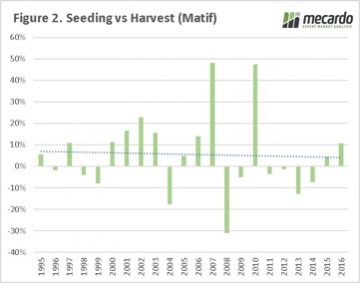

When the Matif contract is examined a different picture emerges. The price during the Australian harvest has been lower only 10 times out of the past 22 seasons, with an average positive change of 5%. However, if we preclude the large changes in 2007 and 2010 the average drops to a meagre 1%.

When the Matif contract is examined a different picture emerges. The price during the Australian harvest has been lower only 10 times out of the past 22 seasons, with an average positive change of 5%. However, if we preclude the large changes in 2007 and 2010 the average drops to a meagre 1%.

Key points:

- Canola acreage in Australia will be increased this year based on our conversations with growers and agronomists.

- The average change between seeding and harvest for the ICE contract is -9%, and for Matif is +5%

What does this mean?

On a historical perspective the ICE November contract has, on average, fallen from its seeding level by 9%, whereas the Matif contract has risen by an average of 5%.

Although from a historical view it doesn’t look overly attractive to get cover during seeding, in the coming year with planting exceptionally high it would still be advisable to get some cover.

A simple risk management strategy is to have cover across a range of periods in order to spread pricing across multiple windows.