Heavier cattle performing better than last year.

Cattle prices managed to hold their ground this week, which is not unusual for this time of year. There are interesting figures for some categories, notably cattle with weight, as they are now more expensive than this time last year.

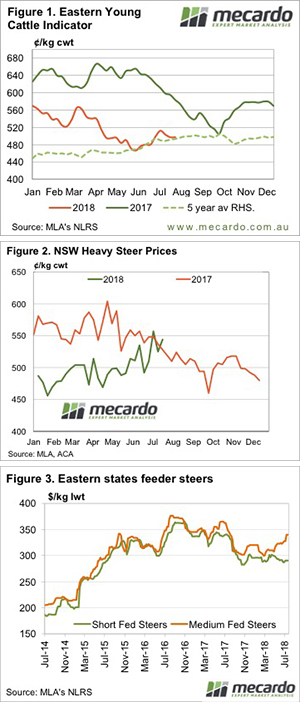

The Eastern Young Cattle Indicator (EYCI) held steady this week, holding on at 497¢/kg cwt and sitting 86¢ below the same time last year (Figure 1). Demand for light young cattle is vastly weaker than this time last year and this is keeping the EYCI at or around the 500¢ mark. We can see in Figure 1 that this level was reached in 2017, but only briefly in October.

The NSW Heavy Steer spent its second week above the 2017 price (Figure 2). Demand for heavy slaughter cattle remains strong, and supply is obviously hard to find, especially for grassfed cattle, as there simply is very little grass out there.

Export Feeder Cattle are also finding plenty of strength, with the Medium-Fed Feeder sitting this week at 340¢/kg lwt (Figure 3). The Medium-Fed Feeder had gained 12% since the start of the year and is now just 5¢ below this time last year.

It is also hard to get weight into cattle for feedlot weights at the moment, hence the very strong prices for heavier feeders.

Export prices, as represented by the 90CL Frozen Cow export price, continue to tick a bit higher this week. The 90CL sits at 579¢/kg swt, 32¢ below the same time last year, so we could even say Heavy Steers are priced better than this time last year.

What does it mean/next week?:

The forecast suggests we’re in for another dry week for NSW and Queensland and as such, there will be little impetus for a rise in the EYCI. Higher rainfall areas of Victoria and SA are receiving something of a normal season and will likely be able to supply cattle as normal this year. Whether the demand for weaner cattle is there at the end of the year will obviously depend on rainfall in the north.