Mixed supply signals as EYCI retreats.

East coast cattle yardings continued to climb this week, spurred on by Victorian producers bringing stock forward. However, a breakdown of the throughput figures indicates that young cattle producers have begun to shy away from offering stock as the Eastern Young Cattle Indicator (EYCI) eased 6.25¢ to close at 480.75¢/kg cwt.

Victorian cattle yarding levels lifted 15% as Southern producers take advantage of relatively firm prices for Trade, Medium and Heavy Steers. All three categories of Victorian Steer prices are marginally ahead of levels set this time last year and with the prospect of pasture decline as the weather warms it seemed enough to get producers to begin presenting cattle for sale.

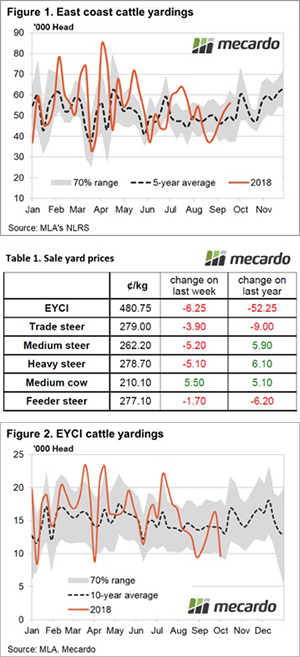

The increased Victorian numbers underpinned a 7% lift in broader East coast throughput levels to see it move toward the upper end of the normal seasonal range in yarding levels for this time of the year with just over 56,000 head changing hands (Figure 1).

The higher volumes across the Eastern seaboard saw most categories of East coast cattle stage a price decline on the week, albeit marginally with falls of 2-5¢ noted. Indeed, Medium cow was the only East coast category to post a lift this week to close at 210¢/kg lwt (Table 1).

Curiously, young cattle yardings bucked the trend of the broader East coast cattle yarding level with the throughput for EYCI eligible cattle declining sharply to see average weekly numbers back below 10,000 head and trending along the bottom end of the normal range (Figure 2).

Year on year price changes was a likely reason for the pullback in young cattle offerings from producers. The EYCI is sitting 10% below levels set this time last season, while most other categories of cattle across the East coast are on par with 2017 levels.

The weaker EYCI isn’t finding support from offshore markets either with the 90CL frozen cow indicator shedding 5% to close at 555.5¢/kg CIF. Relatively firm US beef inventories and the prospect of additional supply out of New Zealand in the coming months is weighing on prices.

Next week

The Eastern coastal regions of NSW, Victoria and Southern Queensland are due for a 25-50mm soaking this week but not much is going to make its way into the middle nor western part of these states.

Adequate rainfall in some areas and the reduction in young cattle yarding numbers may offer some prospect of price support in the short term for the EYCI. However, broader seasonal trends in throughput suggest that cattle prices will continue to face headwinds. A softening 90CL won’t allow the EYCI to gain any real upside momentum either. It seems more likely a case of continued consolidation at current levels with a slight bias to the downside for the short-term outlook.