Mutton back in favour

October has started out pretty well for sheep and lamb markets, with lambs finding solid support and mutton back on the rise. October is traditionally a time of strengthening supply, so we might be seeing another lift in demand.

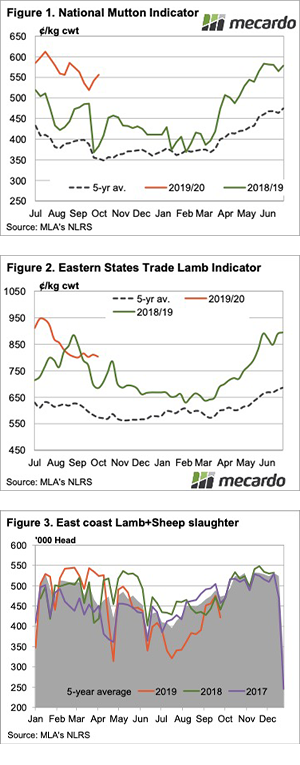

The National Mutton Indicator (NMI) rise last week wasn’t a dead cat bounce, unless it’s one that has lasted two weeks. The NMI gained a further 24¢ this week to move back to 556¢/kg cwt (Figure 1). NSW and Victoria are leading the way, at 588¢ and 598¢/kg cwt respectively, while WA is dragging the chain, at 467¢.

In lamb markets, the Eastern States Trade Lamb Indicator (ESTLI) has spent a seventh week sitting on support at 800¢ (Figure 2). This week the ESTLI closed at 803¢/kg cwt, with NSW at a premium and other states in the 740-760¢ range. Again, WA is the cheapest lamb state, at just 630¢, a significant discount to the east coast.

Traditionally sheep and lamb supply rise sharply at this time of year. After a couple of weeks interrupted with public holidays, figure 3 shows we should see at least a 10% increase in combined sheep and lamb slaughter. We’ve seen this on the five year average, and in each of the last two years.

Theory says for lamb and mutton prices to remain at current levels demand will have to strengthen, and with the commentary on the African Swine Fever ramping up, there is every chance exporters will be able to pay current prices for more stock.

Next Week.

Still no rain on the forecast, so we can expect supplies to at least follow seasonal trends, and maybe increase faster than normal. This could see prices start heading towards seasonal lows, but there is plenty of kill space to fill, and demand seems to be strong at current prices.