Next week we’ll get a handle on supply

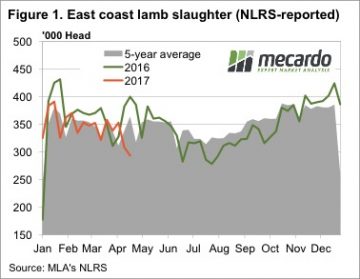

It’s hard to know whether the falling lamb slaughter is due to lower supply, or the short weeks taking some production days out. We’ll hopefully find out next week when we finally get back to full production after three interrupted weeks.

One of the most interesting numbers found this week was MLA’s weekly lamb slaughter for the week ending the 21st of April. Lamb slaughter came in at just 293,342 head, the lowest level since July last year. In the week ending the 21st Lamb slaughter fell 5%, and also sat 5% below the Easter levels of 2016.

One of the most interesting numbers found this week was MLA’s weekly lamb slaughter for the week ending the 21st of April. Lamb slaughter came in at just 293,342 head, the lowest level since July last year. In the week ending the 21st Lamb slaughter fell 5%, and also sat 5% below the Easter levels of 2016.

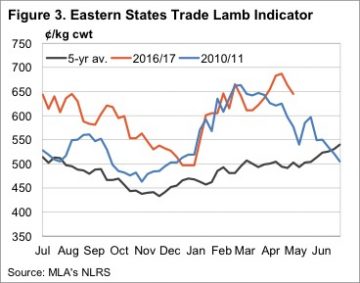

Despite weaker slaughter levels, lamb prices fell last week, and continued to ease this week, the Eastern States Trade Lamb Indicator falling 22¢ and hitting a four week low of 645¢/kg cwt. It will be interesting to see if the ESTLI can find some support at 650¢/kg cwt.

There are some forward contracts out there pitched at 650¢ for May and 660¢ for June and July. This suggests lamb supply might remain tight for some time yet, and we should see the ESTLI bounce over the coming weeks.

Not all lamb prices fell this week, Merino lambs gained 19¢ on the east coast, while light lambs were up 12¢. Neither quite managed to hit record highs, but are not far off at 611¢ and 673¢/kg cwt for Merino and Light lambs respectively.

Not all lamb prices fell this week, Merino lambs gained 19¢ on the east coast, while light lambs were up 12¢. Neither quite managed to hit record highs, but are not far off at 611¢ and 673¢/kg cwt for Merino and Light lambs respectively.

Mutton values also eased this week, losing 21¢ for the week on the east coast to sit at 482¢/kg cwt. Mutton still sits 167¢ above the same time last year, which on a 25kg sheep equates to a very handy $42/head.

The week ahead

It’s unusual for lamb or sheep supply to improve at this time of year, with the only time it has happened being in 2011 when prices started to ease in earnest around this time of year. The difference in the seasons is probably what is going to hold prices this time. In 2011 supply had been low in the previous spring, something we didn’t see this year, and the autumn break was late. This saw more lambs come to market, which are likely to be held this year.