Precipitating a boost in prices

Cattle slaughter has been on the rise, but it was no match for a rainfall led price rally this week. Despite this, the Eastern Young Cattle Indicator (EYCI) remains below the same time last year, though there are still some indicators that are beating their 2017 levels.

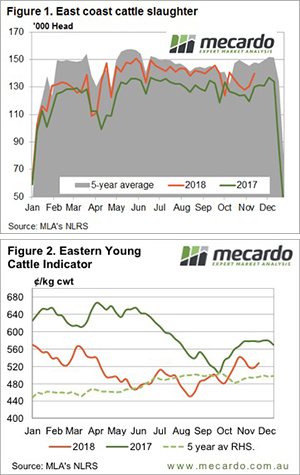

For the week ending the 16th of November, east coast cattle slaughter ramped up to a five-week high of 139,800 head (Figure 1). This was driven by the southern states, most notably Victoria, which hit its highest level since May 2016. NSW slaughter was just shy of its highest slaughter level for the year.

In southern states, the cattle are still flowing. With spring coming to an end, it’s not unusual to see rising slaughter, but in Victoria, slaughter was 20% higher than 2017 last week. It seems the herd rebuild might be on hold in Victoria for the time being.

The story is different in Queensland. While cattle slaughter has risen there in the last couple of weeks, it remains similar to this time last year and below the five-year average.

The EYCI had an uptick this week, gaining 11¢ to 527.5¢/kg cwt. Despite higher slaughter rates, the rain across the east coast helped with demand and tightened the supply of store cattle. The EYCI remains 50¢ below the same time last year.

Interestingly, feeder cattle prices sitting around 300¢/kg lwt are close to the same time in 2017. Despite grain prices being up to 30% higher than last year, the dearth of cattle finished on grass is seeing high grainfed cattle prices continue to support feeder values.

What does it mean/next week?:

There isn’t a lot of rain on the forecast for next week, but the amounts we’ve seen in the last couple of days should be enough to provide continued support for cattle prices. Historically, cattle prices remain steady at this time of year, usually through until Christmas.

However, with higher prices has come higher volatility. We think there is still upside for store cattle but finished cattle values might find a rally a bit harder.