Steady as she goes but some issues on horizon

When the weather is benign the market starts looking for reasons to move. Last night it was the slow pace of wheat shipments leaving US ports. Locally markets have been rather steady, with some short term opportunities cropping up on shipping squeezes.

Figure 1 shows a rather boring CBOT wheat chart. Recent swings in prices have been small on an historical scale. As the volume of supplies dampens any attempts at a real price rally.

Figure 1 shows a rather boring CBOT wheat chart. Recent swings in prices have been small on an historical scale. As the volume of supplies dampens any attempts at a real price rally.

CBOT finishes this week down 2¢ at 423¢/bu, having been as high as 429¢ and as low as 421¢. In our terms, CBOT remains stuck in its $225-235/t range, which while being unexciting on a hedging front, will deliver a price at least 10% higher than the 16-17 harvest.

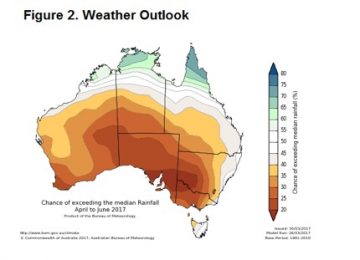

ASX East Coast Wheat Futures are maintaining their premium to CBOT, possibly assisted by the Bureau of Meteorology’s latest 3 month outlook (Figure 2). ASX Jan-18 currently sits at $241/t which is obviously better than current values.

The new ASX contract is deliverable in Victoria, NSW and Queensland, which makes it more attractive to sellers. Even with the spot contract for May at $221/t, there would be an advantage at some Victoria sites in selling futures and going to delivery, rather than taking site bids which equate to prices $5-10 lower.

There has been intermittent interest in Canola, ASW and Feed Barley in recent weeks, with some growers managing $10-20 premium on published bids when buyers are trying to fill ships. If you’ve got wheat in store it’s worth looking at the shipping stem to see when boats are going and trying your luck with offers on Clear, or by talking to buyers or brokers.

There has been intermittent interest in Canola, ASW and Feed Barley in recent weeks, with some growers managing $10-20 premium on published bids when buyers are trying to fill ships. If you’ve got wheat in store it’s worth looking at the shipping stem to see when boats are going and trying your luck with offers on Clear, or by talking to buyers or brokers.

The week ahead

Figure 2 is even making news in international grain wires, with some concern around the sowing of the coming winter crop. It hasn’t done much for prices, but if we do see a late autumn break, spot prices are likely to creep higher as growers use abundant grain in store as a drought hedge.

Our target for hedging new crop continues to be at the $250/t level for wheat, and $500 for Canola, both of which are a little way off. As usual growers are should be hoping that Figure 2 is wrong, and US and or Russian growers get some bad weather during their spring and summer, to take the edge off heavy world supplies.