Supply and demand find equilibrium

The main ovine indicators have found some sort of support in the last fortnight, with the Eastern States Trade Lamb Indicator (ESTLI) spending a second week just above 800¢. Mutton has maintained its position in the 99th percentile.

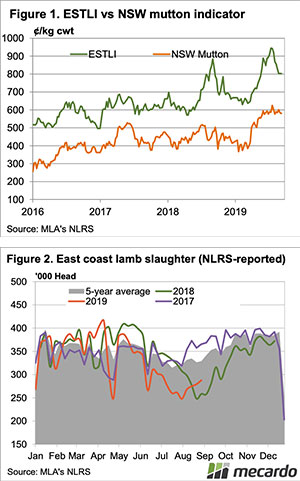

Figure 1 shows the ESTLI remaining steady this week at 803¢/kg cwt. State trade lamb indicators were also relatively steady. Victoria remains cheap, at 750¢, while NSW is at the premium, at 815¢/kg cwt. The quality of trade lambs coming out of NSW is likely better, with bits and pieces of old season lambs are still depressing Victorian yards.

Lamb slaughter continues to creep higher (Figure 2). Mutton supply remains tight, but is still steady. It appears more slaughter space is opening up to accommodate the slow increase in lamb supply.

Mutton prices have spent their fifteenth week above 575¢ in NSW, with similar prices across the east coast. Mutton slaughter was last week 42% below the same time last year, although it has been lower as recently as 2016. It’s hard to see mutton supply increasing, perhaps if the dry spring continues, we’ll see another wave of mutton.

WA prices have found a base, with WA Trade Lambs and Mutton relatively steady at 652 and 435¢/kg cwt respectively. Yardings in the West this week were less than half the same time last year, and it’s not surprising with WA over the hooks rates at 725¢ for lambs and 475¢ for mutton.

Next week

Often the trend with lamb prices is for a rapid fall from the peak, followed by a more gradual decline as we move through spring. The market is set up nicely for this sort of trend, with lamb supply likely to keep increasing as sucker supplies start to come from the south.

There are more showers forecast for areas already going ok this week, but the dry in NSW will continue to creep south. Store lamb prices are likely to be the first to head lower if it does remain