This was a good price in 2015

The slide in cattle prices continued this week, with more help from lower export prices, pushing the EYCI back to two year lows for this time of year. Rainfall across NSW and Victoria doesn’t seem to have helped the cause yet, as supply continues to outweigh demand.

The slide in cattle prices continued this week, with more help from lower export prices, pushing the EYCI back to two year lows for this time of year. Rainfall across NSW and Victoria doesn’t seem to have helped the cause yet, as supply continues to outweigh demand.

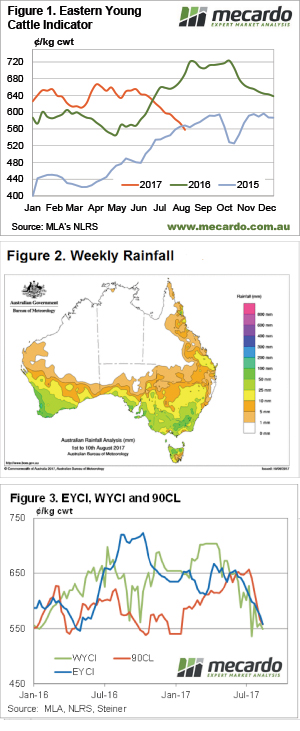

After only recently falling below 2016 levels, the Eastern Young Cattle Indicator (EYCI) this week eased below 2015 levels. The two year low puts the EYCI a very large 134¢, or 19% below the levels of this time last year.

Obviously when the EYCI reached 560¢ back in July 2016, it was happy days for cattle producers. This year prices are still ok, but given they have fallen 14% in 12 weeks, at a time of year when they normally rise, has taken the market by surprise.

There was also some decent rainfall around this week, and for August to date (figure 2). This hasn’t at all translated into any demand, as young cattle prices continue to ease even though yardings haven’t been anything extraordinary.

The 90CL price continued to fall this week, losing a further 10¢ in AUD terms. This is no doubt helping to drag cattle prices lower, as it’s now also lost 14% in 12 weeks. Weakening demand for 90CL beef in the US is apparently the driver, with foodservice not doing so well.

Positives in the cattle market were hard to find this week. The National Heavy Steer Indicator gained 15¢ to move back to 521¢/kg cwt. This was despite the Queensland indicator sitting at 494¢, and there being no quote from any other state.

The week ahead

We are still waiting for cattle prices to find a floor after this very abnormal decline. It’s hard to know if the market will experience a normal spring decline from there, or whether there will be some rain and a subsequent price rise.

Despite the falls in the 90CL export price, there is a little room for upside, especially if the Aussie dollar does the right thing, and it rains.