US market and exchange rate showing some reason for optimism

We have been talking about the spectre of a correction in the Australian

cattle market for some time. The main driver behind any fall in prices, apart from local climatic issues, will be the weakness in international cattle markets. There is some reason for optimism however, with US cattle futures making some sort of a comeback in November and December.

Regular readers will be well aware that while the boom in local young cattle prices is reaching fever pitch at the moment, on an international level it is well and truly over. The US is one of Australia’s major markets for manufacturing beef, as well as a competitor in high value markets of Japan and Korea. As such what happens in the US cattle markets will

generally have an impact on our markets at some stage.

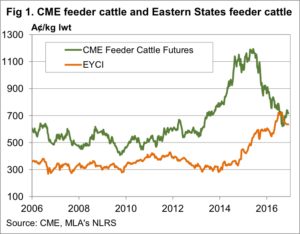

Figure 1 shows how US Feeder cattle futures have tanked since

reaching a peak in July 2015. However, US Feeder do seem to have

found some sort of base, having bounced 12% since hitting a 3 year

low in November. We can also see in figure 1 that the US price rally,

along with a fall in the Eastern Young Cattle Indicator (EYCI) means

that after a brief period at a premium, our prices are back at a discount.

Believe it or not, this is a good thing, it means pressure on prices to move lower will ease.

Additionally the easing Aussie dollar has added further upside to US prices in our terms, Feeder cattle futures have gained 16%, adding support for local prices.

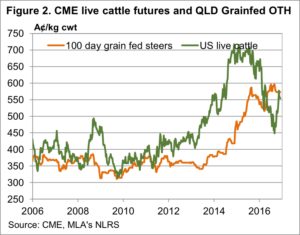

In finished cattle markets in the US the price improvement has been

even more marked. Figure 2 shows US Live Cattle Futures, which is

roughly equivalent to heavy grainfed cattle here, has gained 19.5% in

US terms and 23.5% in our terms. This equates to 100¢/kg cwt in our terms,

and basically means that US beef that competes with ours in Japan and

Korea is more expensive than it was two months ago.

Further encouragement for local prices can come from the fact that

Queensland Grainfed Cattle prices have historically spent long periods at or

around parity with US prices. Under a tight supply scenario, there is little

pressure on heavy grainfed cattle prices to fall.

Key points:

- US Cattle prices have made a recovery from the 3 year lows seen in November.

- The falling Aussie dollar has added more strength to the US equivalent prices in our terms.

- If US cattle prices remain strong they should provide support for Australian values.

What does this mean?

Before the rally in US cattle prices at the end of 2016 we were concerned about downside for

heavy grainfed, and grassfed cattle. Eventually weaker heavy cattle prices would translate into

feeder and young cattle prices. However, the pressure on heavy cattle values has eased somewhat,

and while the market might struggle to move higher without help from the US, downside is limited

as long as US prices don’t tank again.

Continued strong heavy cattle prices will continue to support young cattle prices, as long as feed

remains abundant and cheap, which it should – at least in the short term.