Beef and Lamb spreads – saleyard to retail.

Surging saleyard lamb prices in the Eastern states have seen the spread between the Eastern Young Cattle Indicator (EYCI) and the Eastern States Trade Lamb Indicator (ESTLI) widen toward historical extreme levels in recent weeks. This analysis piece looks at the historic behaviour of the EYCI to ESTLI spread and what it can tell us about beef and lamb prices at a retail level.

The ESTLI has reached beyond the 830¢/kg cwt level recently, while the EYCI continues to languish, staging a drift towards a three year low of 444¢/kg cwt. The contrasting behaviour of these saleyard lamb and cattle price indicators has pushed the percentage spread differential between the EYCI and the ESTLI to a 45.7% discount. That is, at the saleyard, young cattle on the East coast are currently trading 46% below trade lamb on a carcass weight basis (Figure 1).

The historical trend in the percentage spread between the EYCI and the ESTLI highlights that it is not uncommon to see young cattle prices run at a discount to trade lamb at the saleyard. Indeed, analysis of the trend in the weekly spread since 2001 shows that the long-term average EYCI to ESTLI spread sits at a discount of 10.5% (Figure 2). That’s not to say that there aren’t times when young cattle prices achieve a premium to trade lamb. Indeed, as the 70% range area highlights, since 2001 the EYCI to ESTLI spread has spent 70% of the time fluctuating between a discount of 29% to a premium of 8%.

Analysis of the current EYCI to ESTLI percentage spread shows that the 45.7% discount is nearing historically low levels, with the most recent widening of the discount spread at 46.2% occurring during March of 2014 (which was the widest discount spread achieved so far). According to the historic statistical measurement of the spread behaviour, movements below a discount of 47% or above a premium of 26% would be considered extreme, as identified by the 95% range boundaries.

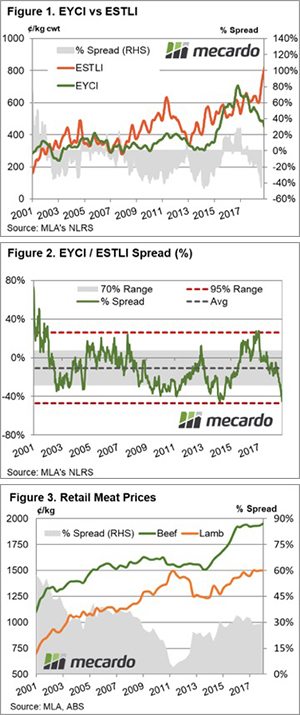

Interestingly, the percentage spread analysis of the average quarterly retail price of lamb and beef as reported by the Australian Bureau of Statistics demonstrates that since 2001 beef commands a spread premium over lamb and has never traded at a spread discount (Figure 3). At a retail level, the beef to lamb percentage spread has averaged a 30% premium over the 2011 to 2018 period.

The narrowest the retail beef to lamb spread has been was a 4% premium that occurred during the June quarter of 2011. At this time saleyard young cattle prices were running at a 31% discount to trade lamb. During March of 2014 when the saleyard discount between beef and lamb prices were at their widest point, at a 46.2% spread, the retail spread of beef to lamb was at a comfortable 24% premium. Similarly, as the EYCI to ESTLI spread widened significantly towards an extreme 46% discount at the saleyard in recent times, the retail spread of beef to lamb has remained firm at a 30% premium.

What does it mean?

At a retail level at least, this reinforces how much we love our beef. Despite times when cattle prices at the saleyard are trading at a significant discount to lamb, the discount never translates to cheaper beef than lamb (across the average price of cuts) for the consumer.

During the 2017 season, Australians consumed 26.4 kg of beef compared to 8.6 kg of lamb on a per capita basis. Domestic demand for beef is three times that of lamb and is the likely reason why retailers can continue to demand a premium for beef over lamb, despite paying more for lamb than beef at the saleyard.

Key points:

- Saleyard spreads between the EYCI and ESTLI have widened to historic extremes with the EYCI currently trading at a 45.7% discount to the ESTLI.

- Historically, since 2001 the EYCI has averaged a discount spread to the ESTLI of 10.5% and has fluctuated between a 29% discount and an 8% premium spread for 70% of the time.

- The discount spread between cattle and lamb at the saleyard doesn’t translate to a discount in the average beef and lamb price across all cuts at a retail level.