Cattle market a paradox

Cattle markets managed to edge higher this week, despite stronger supply. The Eastern Young Cattle Indicator (EYCI) moved back above 500¢ and within a tick of the price this time last year. It’s the spreads in restocker values we are interested in this week though.

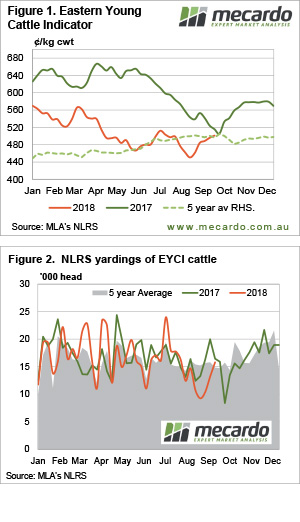

Cattle markets managed to edge higher this week, despite stronger supply. The Eastern Young Cattle Indicator (EYCI) moved back above 500¢ and within a tick of the price this time last year. It’s the spreads in restocker values we are interested in this week though.

Figure 1 shows the EYCI taking its rally up 11% from the lows to hit 501¢/kg cwt. Last year the market reached its low of 504¢ in early October and given the price of grain, and the lack of grass, it is remarkable to see it at similar levels.

Even with young cattle supply lifting to a six week high (Figure 2) prices managed to continue to lift. Delving a bit deeper into the EYCI data we can see that the proportion of yearling cattle has risen in recent weeks. As we keep saying, demand for finished cattle remains good so those hitting the market are well sought after, which is dragging the EYCI higher.

It was the quotes for restocker steers in MLA’s data which caught our eye this week. In Victoria restocker steers were quoted at 229¢/kg lwt. In Queensland restocker steers were 274¢. You would be forgiven for thinking Victoria was in drought, and things were okay in Queensland. We know it is currently the opposite scenario, with at least parts of Victoria faring okay. It might the depressing rainfall outlook which is limiting demand for young cattle.

WA still has the best cattle prices in the country. MSA Yearlings are quoted at 565¢/kg cwt, 37¢ stronger than their NSW counterparts. Normally finished cattle start to flow in the West at this time of year, which could see some price adjustments coming up.

What does it mean/next week?

Rain will remain scarce over the coming week, with only a thin strip of northern NSW coastline seeing anything meaningful. It’s starting to look like supply is going to be fairly stagnant, with few cattle left to really flood the market. This means prices might stagnate as well, with obvious strong upside when it finally does rain properly.