EYCI nearing price resistance with supply dearth still to bite

Cattle supply is expected to wane, and prices are already on the rise. It is still worth having a look at how the tighter cattle supply is likely to play out on a seasonal basis, and what this might mean for prices.

Last week we took a look at Meat & Livestock Australia’s (MLA) Cattle Industry projections on a broad basis, and this week we delve into what this will mean for prices. While the sheep and lamb prices are tightly tied to supply, cattle are a bit more complicated. The global nature of the cattle market means our prices are strongly impacted by supplies from other exporting countries.

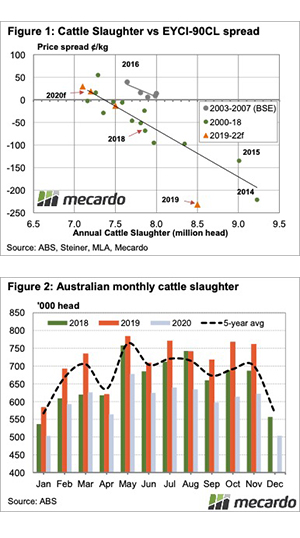

As such, we’ve found cattle prices here are a result of export prices and supply. Figure 1 demonstrates how the level of cattle slaughter governs the discount or premium of the Eastern Young Cattle Indicator (EYCI) to the 90CL Frozen Cow price, exported to the US.

We can see that in 2019, despite strong slaughter, the EYCI discount to the 90CL deviated significantly from the trend line. This was likely a factor of strong export prices and very weak restocker demand from the drought.

So far in 2020, the EYCI discount to the 90CL has narrowed, last week it was at 53¢, with the 90CL at 715¢/kg swt. This week, the discount is likely to narrow further, with the EYCI at 692¢ on Wednesday.

There is no guarantee the volatile export prices will stay at 700¢. Assuming it does, and the EYCI moves to a 20¢ premium, it gives the EYCI another 40-50¢ upside before it gets historically ‘expensive’ relative to export prices.

There will always be seasonality in livestock prices, and variations in supply generally govern how prices range around the average. Figure 2 shows how the MLA forecast slaughter of 7.2 million head will hit the market if five-year seasonality holds.

Cattle slaughter is expected to be over 10% lower than last year in all months. October to December, which were strong slaughter months in 2019, are expected to take the biggest hit, with 17-20% fewer cattle expected to be slaughtered.

What does this mean?

Cattle prices have rallied so strongly they have nearly made up all the ground we would expect them to, relative to export prices. There could still be a further upside, but once the EYCI moves past export values, price resistance starts to mount.

The seasons have been far from normal recently, but rainfall might signal some sort of return. Once prices level out there could be a return to normal seasonality, with winter peaks and summer declines. The peak EYCI could be as high as 800¢, while the low shouldn’t be much less than current prices, providing the rain keeps coming.