Heavy steer spreads to EYCI during a favourable season.

Key points:

- So far during 2017 heavy steer spreads to the EYCI have been trekking along the lower end of the normal range for East coast cattle.

- The spread pattern in each state has been roughly mirroring the pattern set by the 2011/12 average pattern, the last time we experienced a favourable season along the East coast.

- Young cattle are likely to continue to outperform finished lines for the next six months but the discount spread is likely to narrow as we transition into a drier climate into 2018.

During a favourable season optimism runs high among restockers and opportunistic cattle traders supporting demand and prices for store/young cattle. The added buying competition between the three main purchasing groups (restockers, lot feeders and processors) will often see the Eastern Young Cattle Indicator (EYCI) outperform the price patterns for finished lines, as there is really only one buyer type for fat cattle – the processor. This piece will take a look at what can be expected for the spread pattern between heavy steers and the EYCI along the East coast for the next six months.

During a favourable season optimism runs high among restockers and opportunistic cattle traders supporting demand and prices for store/young cattle. The added buying competition between the three main purchasing groups (restockers, lot feeders and processors) will often see the Eastern Young Cattle Indicator (EYCI) outperform the price patterns for finished lines, as there is really only one buyer type for fat cattle – the processor. This piece will take a look at what can be expected for the spread pattern between heavy steers and the EYCI along the East coast for the next six months.

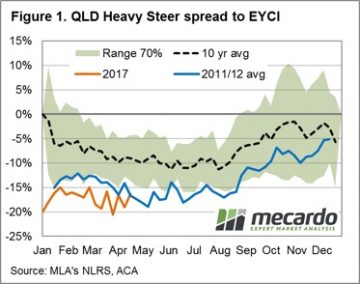

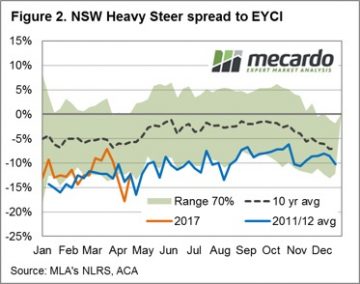

The most recent favourable season for cattle traders along the East coast occurred during 2011/12, on the back of widespread rainfall that began in 2010. Each figure accompanying this analysis piece displays the spread pattern for heavy steers compared to the EYCI for 2017 for Queensland, NSW and Victoria. Overlaid with the spread pattern for the current season is the average spread pattern for 2011 and 2012, along with the long term spread pattern and the “normal” range (highlighting where the spread has fluctuated for 70% of the time over the last decade).

Interestingly, so far for the 2017 season the spread pattern in all three states has been following a similar trajectory to the 2011/12 average pattern. In addition, each state’s spread pattern for this season is trending close to the lower end of the 70% banding, reflecting that the favourable conditions have supported young cattle prices more than the price for finished cattle. Perhaps somewhat unsurprisingly the state that was hit hardest by the most recent cattle turnoff, Queensland, is experiencing the widest spread between young and finished cattle as the requirement to rebuild the herd is likely to be most evident in that region.

Interestingly, so far for the 2017 season the spread pattern in all three states has been following a similar trajectory to the 2011/12 average pattern. In addition, each state’s spread pattern for this season is trending close to the lower end of the 70% banding, reflecting that the favourable conditions have supported young cattle prices more than the price for finished cattle. Perhaps somewhat unsurprisingly the state that was hit hardest by the most recent cattle turnoff, Queensland, is experiencing the widest spread between young and finished cattle as the requirement to rebuild the herd is likely to be most evident in that region.

The Queensland heavy steer to EYCI spread normally experiences a trough during Winter and, based off the current pattern, a widening of the discount spread to 20-25% during the middle of the year would not be out of the question. The NSW heavy steer to EYCI spread is likely to remain fairly stable through the middle of the season, ranging between a 7-12% discount for the next six months. The Victorian heavy steer spread normally follows an opposite pattern to Queensland, on account of the different seasonal factors present in the north/south of the country, and is anticipated to reach a peak during Winter near the 3-5% discount level.

What does this mean?

It is likely the spread patterns for each state will continue to trek along the lower end of the 70% band for much of the second half of the year. However, as the confidence level on longer term climate predictions for the 2018 season grows into the later stages of 2017 spreads may begin to return to more normal levels, particularly if the transition from a wetter to drier climate cycle becomes more evident.

It is likely the spread patterns for each state will continue to trek along the lower end of the 70% band for much of the second half of the year. However, as the confidence level on longer term climate predictions for the 2018 season grows into the later stages of 2017 spreads may begin to return to more normal levels, particularly if the transition from a wetter to drier climate cycle becomes more evident.