Look at them go

A good winter outlook, moisture in the soil and the lowest yarding levels all season have seen cattle prices hold ground this week for most categories. Although over the longer term it has been a good run for prices all year with average monthly price gains since January between 18%-35% across the CV19 reported categories.

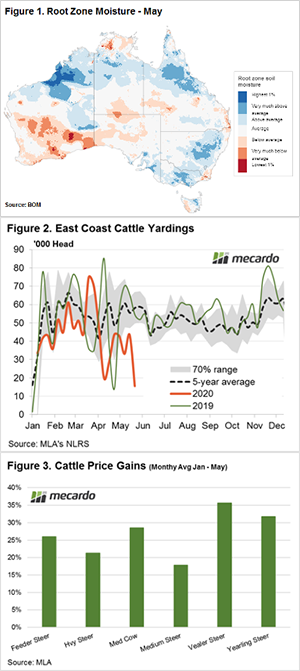

The Bureau of Meteorology released their end of May three-month climate outlook yesterday and it shows a 60-80% chance of a wetter than average winter is expected for much of Australia. Furthermore, the very much above average root zone soil moisture seen during May across large areas of eastern NSW is giving some confidence back to producers impacted by the dry conditions seen in 2019 (Figure 1).

East coast cattle yarding levels have eased to the lowest weekly point this season with only 15,558 head presented for the week ending 22nd May, which represents a 73% reduction from the five-year average trend for this time in the year (Figure 2).

A breakdown of the three key east coast states shows cattle yarding in Queensland is running 63% under the five-year trend, while Victoria is at 73% below average levels. However, the state really dragging down the total east coast yarding numbers is NSW with a mere 3,841 head presented last week, 83% below the seasonal trend for this time in the year.

The combination of a favourable climatic situation and tight supply lent support to some cattle categories this week. The MLA CV19 for National Vealer Steer indicator showing the best result with a weekly gain of 4.4% to close at 420¢/kg lwt. National Medium Steer was up 2.4% and Medium Cow managed a 1.2% lift.

The National Heavy Steer softened 1% on the week to close at 351¢/kg lwt and Yearling Steers were off by 4.5%. However, a look at price gains since the start of the season highlights how 2020 has turned to favour producers with gains from 18%-35% across all reported categories (Figure 3).

What does it mean/next week?’

As outlined in last week’s market comment the improving picture in US Live Cattle Futures markets (up nearly 4% this week and closing at 101.6US¢/lb overnight) along with the combination of tight local supply and a good rainfall forecast all bodes well for cattle producers as we head into winter. Expect domestic cattle prices to continue to be supported over the short term.