Slaughter still running hot as is 90CL.

Cattle markets largely steadied this week, as the yo yo which has been young cattle values stopped to take a look around. Slaughter rates have been running hot, keeping a lid on prices despite the 90CL hitting a 4 year high.

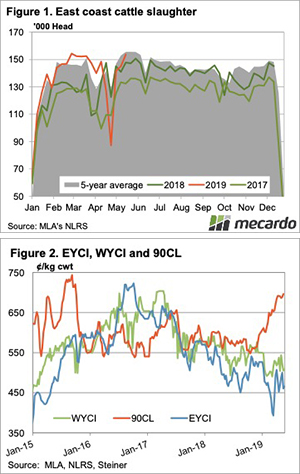

Just when we thought the heavy supply of cattle in general was on the wane, slaughter rates jumped higher last week. The 153,569 (figure 1) head of cattle slaughtered last week was the second biggest week for the year.

In NSW and Queensland female slaughter rates remain high, sitting 14% and 16% above the same week last year respectively. We know high female rates can’t go on forever, and with total slaughter will have to fall at some stage.

Lower prices seems to have had some impact on supply at saleyard level. Young cattle yardings in Eastern Young Cattle Indicator (EYCI) yards fell by 18%, and this helped push the EYCI 8¢ higher to 468.75¢/kg cwt (figure 2).

With the Aussie dollar falling below 69US¢ this week the 90CL in our terms received a 10¢ boost. Sitting at 696¢/kg swt, it has been 4 years since the 90CL was this strong. Strong beef export prices are no doubt helping keep prices reasonable in the face of heavy supply, but will also contribute to a strong rally if and when supply tightens.

The WA Young Cattle Indicator (WYCI) is holding its premium to its East Coast counterpart. There are better premium in finished cattle market in the west however, with over the hooks rates of 540-580¢ for steer easily beating the 520-530 available ‘over east’. WA prices are a good indication of what the export market can pay.

What does it mean/next week?:

While some key cattle areas in Victoria and South East SA are going to get some more rain this week, the rest of the country is going to stay dry. As such we don’t expect any rapid rallies in young cattle prices, but finished grassfed cattle could continue to creep higher.