USDA Day

A relatively downbeat week in the grain trade, with the world watching and waiting for the next big driver of pricing. The big data release for the week was the USDA world agriculture supply and demand estimates.

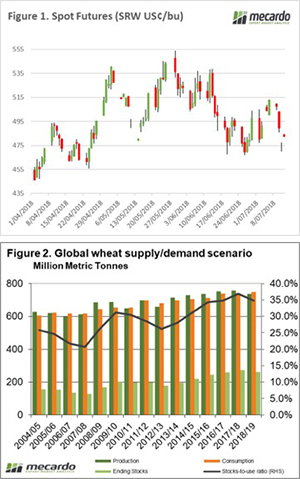

There has been a high degree of volatility in the past week as traders scope for telltale signs of weather impacted yields in the northern hemisphere. The market has recovered A$5 overnight, but week on week the wheat futures market is down 6% or A$14 on the spot contract (Figure 1).

The July USDA report was released overnight. The report called major reductions for wheat production around the world. The global end stocks for the coming season were dropped to 250mmt, the lowest since 2016/17 (Figure 2).

The USDA has lowered consumption of wheat by 2.3mmt, however, this was more than offset by falls in production. Dry conditions around major crop growing regions are the driver of this downward movement in Australia (-2mmt), EU (-4.4mmt), Russia (-1.5mmt), Ukraine (-1mmt).

This report was generally bullish in nature and points towards a tightening global wheat market. Although global wheat stocks will still be the second highest on record, production by the main exporting nations is slipping.

What does it mean/next week?:

This week will see more certainty as the northern hemisphere harvest progresses. There are a few tenders in the next few days which will give some indication of pricing signals.

Locally in Australia VIC, SA & WA are forecast to receive reasonable rainfall events in the next eight days. It however, looks like NSW is set to miss out.