Waiting ….. waiting… waiting.

Key Points

It feels like the Australian grain industry is operating with a sense of calm despite the global chaos regarding China and COVID-19. The cause for this calm in Australia is the rainfall to date or the “seasonal conditions”.

Focusing on the domestic front, growers are content to focus on growing a crop and leaving sales to later. This is not an unusual situation at this time of the year, and with the best seasonal conditions in a couple of years across much of the grain area, the expectation of a good crop is cautiously in consideration.

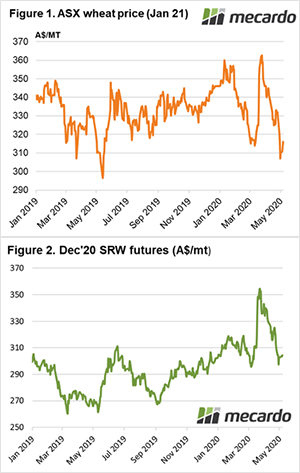

A look at the difference in price between “old crop”, that is 2019/20 production, and “new crop”, 2020-21 production, helps to tell the story both in regard to price and supply.

Using ASW delivered Melbourne prices from feed millers as the reference, prices bid today are circa $370 per tonne, however, the forward bid for the crop in the ground is $60 lower.

This reflects the drought affected supply of last year with stocks tight to meet domestic demand this year, however, looking ahead consumers are expecting (hoping) that a big crop will lower their costs. They, therefore, have little appetite to secure supply by forward purchasing, content with the outlook for production and the sufficient supply expected.

For Barley the “old crop – new crop” spread is $15. The tighter spread compared to wheat is a result of the recent China tariff announcement which took the wind out of the sails of any unsold barley closing the gap to “new crop” prices. You can read more about these impacts on Mecardo here.

So the summary to buyer and seller activity is wrapped up in the uncertainty worldwide and the Australian crop expectation. Growers are resisting the lower bid prices and following reports from other grain-producing countries of murmurings of concern regarding weather.

On the other hand, buyers have little perceived domestic supply risk so are not providing any aggressive bidding and will remain calm while the good growing conditions persist.

Regardless of which way the weather goes, it will change sentiment in the coming months. Either buyers will begin to accumulate if conditions tighten or growers will start a selling program if their confidence in the season builds.

Next week?

The talk about weather this week was dominated by the widespread frosts across eastern Australia. The fact that little concern was raised by growers reiterates the level of comfort they have with soil moisture levels (generally speaking).

The focus on rain will begin to take on more urgency coming out of the winter, with spring rain now the key element in what the eventual crop production figure will look like.