Will lamb suffer a post Australia Day Hangover?

Despite the issues with slaughter capacity in South Australia it seems that we once again managed to achieve a slaughter spike in the middle week of January. In some years the weaker demand in early February has led to weaker prices, but last year it was met with weaker supply, and strong prices.

Despite the issues with slaughter capacity in South Australia it seems that we once again managed to achieve a slaughter spike in the middle week of January. In some years the weaker demand in early February has led to weaker prices, but last year it was met with weaker supply, and strong prices.

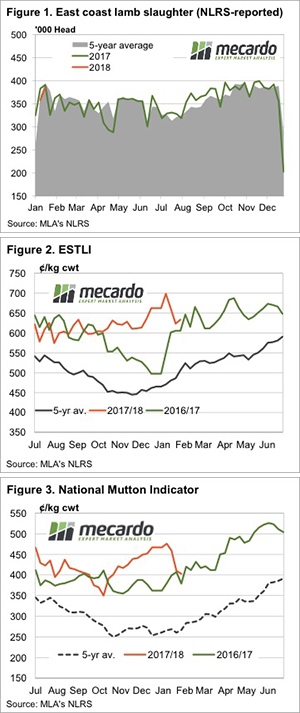

Figure 1 shows what seems quite remarkable under the circumstances. With 55,000 head of sheep and lamb slaughter capacity taken out by the TFI fire in early January, east coast processors have killed just 1.6% fewer lambs in the week ending the 19th of January.

Prices did fall in that same week, which could be put down to a bit less competition, and perhaps strong over the hooks bookings in response to concerns about slaughter capacity. Last week we saw steadier prices (figure 2) as fewer lambs were yarded in response to lower prices.

Historically we see a small fall in prices at the end of January, followed by a gentle rally as lamb supply becomes tighter. Strong spring slaughter would suggest the supply trends should be similar this year, as long as demand holds on.

Mutton prices have suffered in January, and this might be where reduced slaughter capacity is hitting home. The National Mutton Indicator started the year at 470¢, and has since lost 14% to be sitting back at 400¢/kg cwt, the lowest price since early November. This could turn around as processors turn back to mutton as domestic lamb demand weakens.

What does it mean/next week?:

The lamb market seems to have found a base at the moment, at prices a little higher than this time last year. Don’t be surprised to see values track sideways from here, with a bit of volatility as the supply of finished lambs fluctuates.

There appears to be more upside for mutton given the dramatic fall it has seen, and what should be tightening supply. Some rain through NSW would obviously help bolster prices, but it looks like Queensland is going to be the beneficiary this week.