Key points:

- The most recent peak in NSW mutton prices

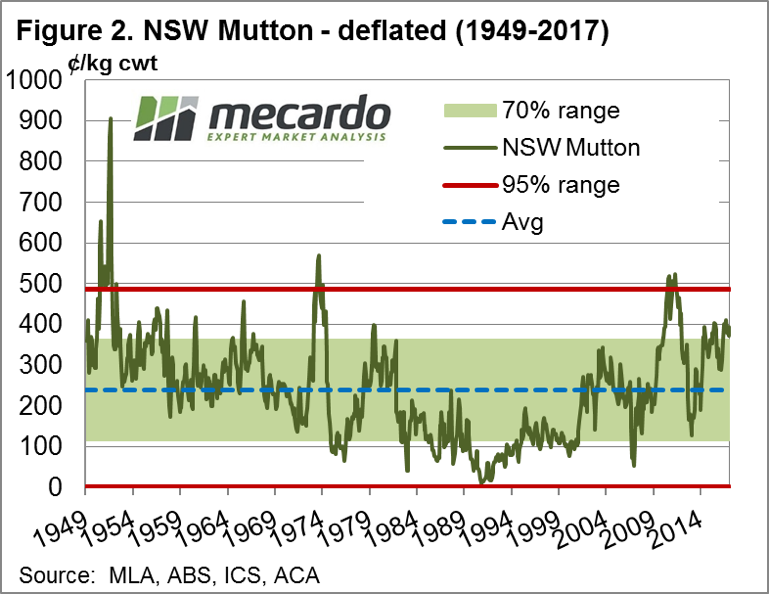

in deflated terms (current day dollars) occurred during April 2011 at 523¢/kg cwt

in deflated terms (current day dollars) occurred during April 2011 at 523¢/kg cwt - The long term average deflated NSW mutton price is 239¢ based on data going as far back as 1949

- Since 1949, NSW mutton prices have spent 70% of the time between 115¢-362¢ and 95% of the time between 0¢-485¢

Last week Mecardo released an article on long term deflated prices for the Eastern States Trade Lamb indicator (ESTLI) and this week we have published a similar analysis focusing on long term mutton prices, looking at NSW mutton prices since 1949.

Click here to read the deflated ESTLI article.

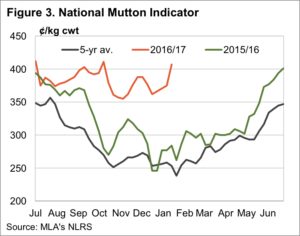

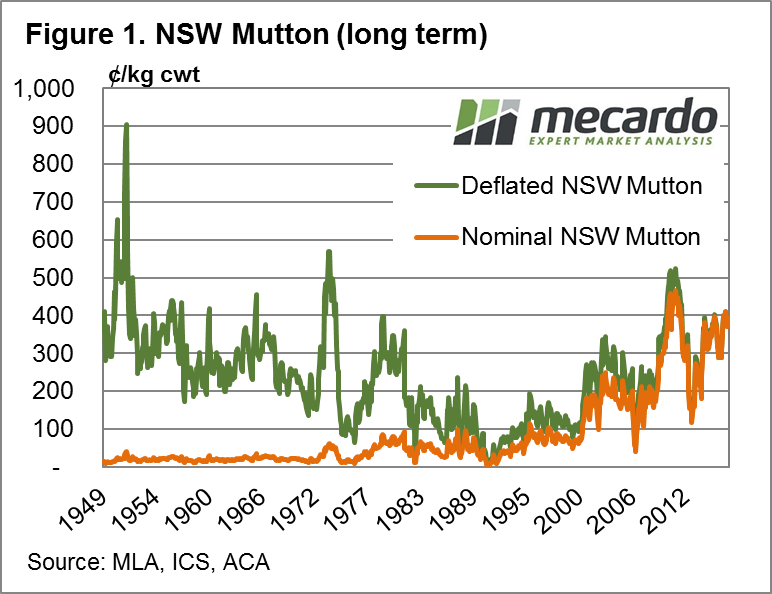

Figure 1 shows the price pattern for both nominal and deflated average monthly NSW mutton prices going back to 1949. Clearly, the 2016 season was a good one for mutton prices and the 2017 season bodes well with the NSW mutton January average of 394¢/kg cwt just sitting 15.4% shy of the nominal average monthly peak that occurred during April 2011 at 466¢. In deflated terms the current mutton prices are holding up well too with a deflated peak in 2011 at 523¢, not too far away from the current level.

Indeed, figure 2 highlights just how well mutton prices have been in current day dollars with the market sitting well above the long term deflated monthly average of 239¢/kg cwt – (blue dotted line). The green 70% range between 115¢ – 362¢ shows were deflated mutton prices have traded for 70% of the time since 1949 and the red lines show the range that encompasses 95% of the variation in price (0¢-485¢/kg cwt) over the same time frame.

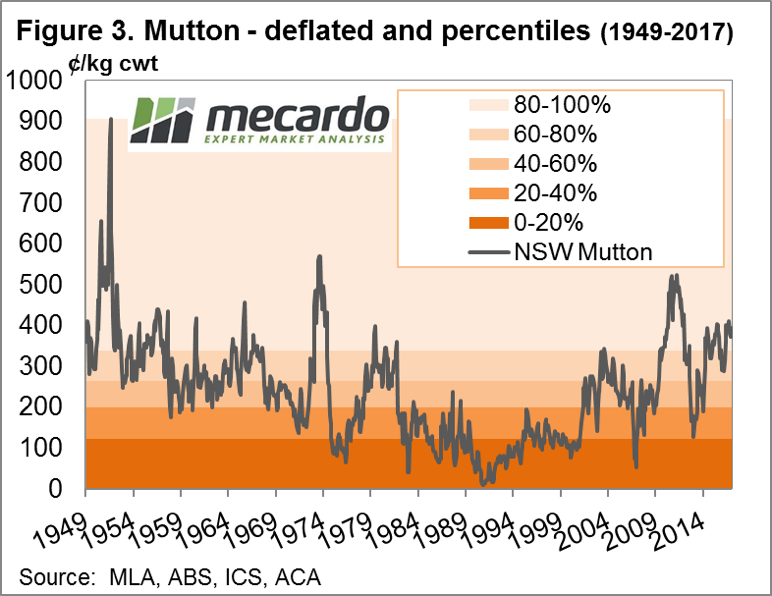

Figure 3 displays the same deflated mutton  price series overlaid with percentile ranges which shows that the current average monthly NSW mutton price has remained in the 80-100th percentile range since April 2016. Unquestionably, mutton prices are holding firm with the January average of 394¢ sitting at the 90th percentile when compared to the deflated price data series since 1949.

price series overlaid with percentile ranges which shows that the current average monthly NSW mutton price has remained in the 80-100th percentile range since April 2016. Unquestionably, mutton prices are holding firm with the January average of 394¢ sitting at the 90th percentile when compared to the deflated price data series since 1949.

What does this mean?

As outlined in the “Mutton hitting the ceiling” article from last week (see link above) there is a case for mutton prices continuing to firm into the 2017 season. While the deflated data suggest we are at reasonably high historic levels there have been times in the past when mutton prices were higher in real terms.

NSW mutton prices wouldn’t be considered to be at extremely high levels until above 485¢ and have reached as high as 523¢ (in current dollar terms) within the last five years, so mutton prices near or slightly above 500¢ this season aren’t out of the question.