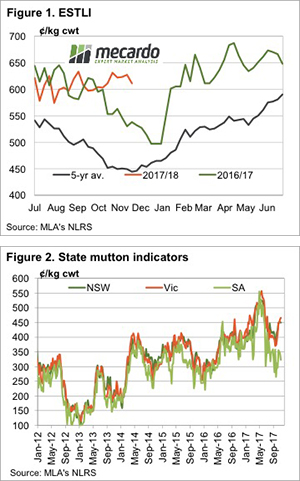

Unseasonal rain will have an impact on sheep markets. This week it had an impact even before it fell, with the Eastern States Trade Lamb Indicator rallying back to 613¢/kg cwt this week. The unpredictable weather might see more surprises yet.

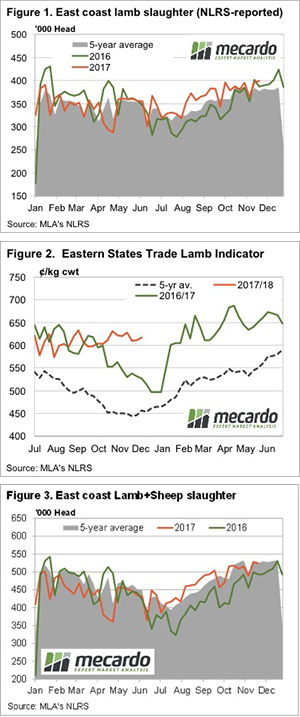

The supply, demand and price equation is still not adding up relative to last year. Figure 1 shows that to the end of last week east coast lamb slaughter hit its 2017 high, just shy 400,000 head. Lamb slaughter was 3% higher than the same week last year, yet the ESTLI remained 17% higher. We keep talking about it, but lamb demand is very strong.

For sheep the equation is similar, but the lift in demand is more dramatic. Last week 18% more sheep were slaughtered than this time last year, yet prices were 14% higher. Total sheep and lamb slaughter for last week was 6%higher than this time last year, and just shy of a two year record (figure 3).

Interestingly however, total sheep and lamb slaughter is right on the five year average. This tells us there is slaughter space available, it just needs to come back online, and at current prices, export demand needs to be strong enough.

In the west lamb prices maintained their strength. At 578¢/kg cwt, the WATLI is 100¢ stronger than this time last year, and not far of the ESTLI. Restocker lambs remain cheap however, at 508¢/kg cwt, compared to east coast at 680¢/kg cwt, and this is encouraging the shipping east. Lambs from WA can be landed in eastern Victoria around $10 cheaper than the local price.

The week ahead

The forecast for the coming days is for plenty of rain. This is the time of year when lamb yardings peak, and processors rely more heavily saleyard supplies than usual. Disruption to saleyard supply due to rain will be hard to replace with direct consignments. This means we could see a short term spike in lamb prices next week as processor battle it out for supply.

After weeks of a glowing market that seemed to keep on rising with record on record, the peak was finally reached and the market edged over the other side. Nearly all categories and microns across the country retracted on the week, however it wasn’t enough to cause too much concern.

After weeks of a glowing market that seemed to keep on rising with record on record, the peak was finally reached and the market edged over the other side. Nearly all categories and microns across the country retracted on the week, however it wasn’t enough to cause too much concern.

Meat and Livestock Australia (MLA) seem to have sorted out the differences with processors who were holding back data slaughter data. For the last couple of week’s slaughter data has confirmed what we thought, cattle supply has been tight.

Meat and Livestock Australia (MLA) seem to have sorted out the differences with processors who were holding back data slaughter data. For the last couple of week’s slaughter data has confirmed what we thought, cattle supply has been tight.

The South Australian Greens have extended the moratorium on GM in their state and over the past few weeks the mob at Mecardo have been investigating the claim made by the Greens that the GM ban, and their clean, environmentally sustainable image, provides a price premium benefit to SA producers. There has not been any sign of a premium on Canola, nor in mutton and lamb. This time we try to find it in cattle.

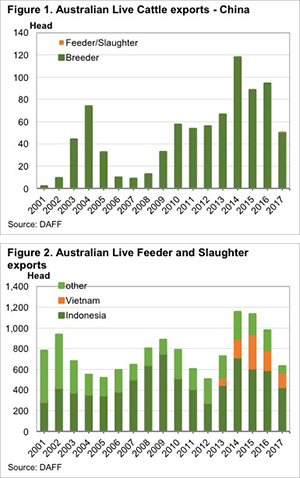

The South Australian Greens have extended the moratorium on GM in their state and over the past few weeks the mob at Mecardo have been investigating the claim made by the Greens that the GM ban, and their clean, environmentally sustainable image, provides a price premium benefit to SA producers. There has not been any sign of a premium on Canola, nor in mutton and lamb. This time we try to find it in cattle. According the Australian Livestock Exporters Council (ALEC) it was agreed last week that China are going to cut the 10% tariff on live feeder and slaughter sheep and cattle imports by January 2019. Is this a big deal, or not?

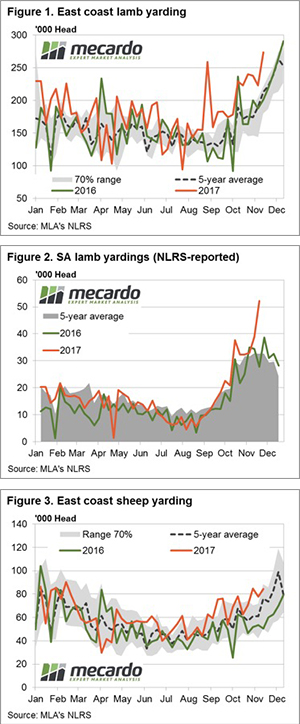

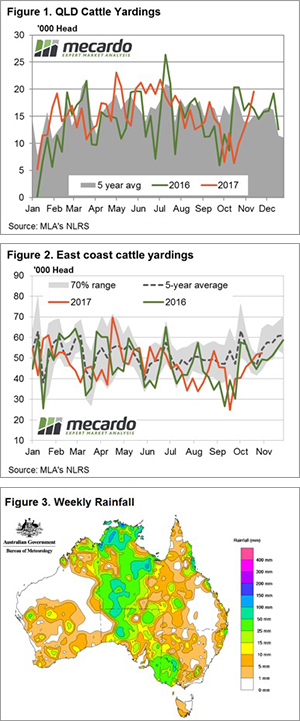

According the Australian Livestock Exporters Council (ALEC) it was agreed last week that China are going to cut the 10% tariff on live feeder and slaughter sheep and cattle imports by January 2019. Is this a big deal, or not? Figure 1 shows the steady rise in Queensland cattle yardings since mid-October and based off last week’s figures we saw another 27% gain in cattle at the saleyards this week. Queensland Restocker, Feeder, Vealer, Medium and Heavy Steers all fetching the strongest prices for their categories across the country this week, so it is probably no surprise that we are seeing producers bring forward supply in the Sunshine State.

Figure 1 shows the steady rise in Queensland cattle yardings since mid-October and based off last week’s figures we saw another 27% gain in cattle at the saleyards this week. Queensland Restocker, Feeder, Vealer, Medium and Heavy Steers all fetching the strongest prices for their categories across the country this week, so it is probably no surprise that we are seeing producers bring forward supply in the Sunshine State.

{kind=link}