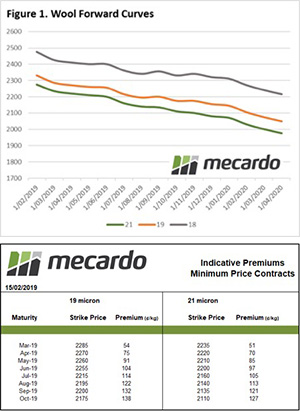

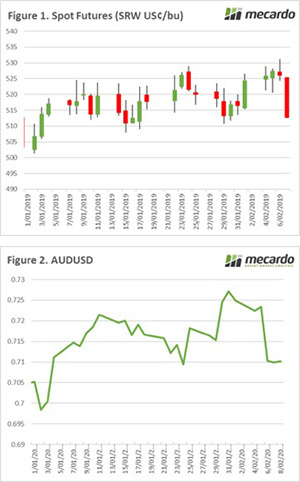

An interesting trend has emerged this week in the auction market, where we’ve seen continual heightened prices across all micron categories. When coupled with the Aussie dollar on a continued downwards trend, one could expect that the forwards market could see more and more action in the coming weeks.

In the 18 micron category, one trade was dealt for June with the agreed price of 2350¢/kg.

In the 19 micron category, six trades were dealt. One was agreed for next month for 2285¢/kg. Two trades were dealt for May between 2240¢/kg and 2250¢/kg. Two trades were made for later in the year, November and December both agreeing at 2125¢/kg. The remaining trade was made for February next year for 2085¢/kg.

In the 21 micron category, two trades were dealt for April, one for 2200¢/kg and the other for 2220¢/kg.

While the Aussie dollar did rally slightly at the end of the week, the downward trend is still evident. Throughout the time that this remains the case, activity from overseas buyers should be higher. The forward market has been very active for several weeks now, generally ignoring the fluctuating Aussie dollar value. This could hint that supply might still be a concern looking into the near future, but also could reflect an overseas comfort with the broader picture of Aussie dollar levels and trends.

For this weeks’ article investigating wool supply issues in the north see here

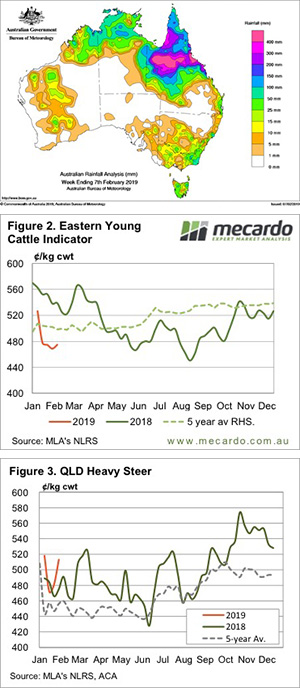

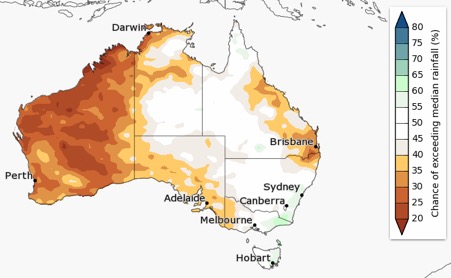

The bureau of meteorology has released its three month climate outlook. It doesn’t look good for Queensland and the West. After a fantastic year where WA produced a 17.5mmt crop, pre season rainfall has a limited chance of exceeding the median. This will put a dampener on expectations for the coming season. However, I have a few thoughts when it comes to this projection:

The bureau of meteorology has released its three month climate outlook. It doesn’t look good for Queensland and the West. After a fantastic year where WA produced a 17.5mmt crop, pre season rainfall has a limited chance of exceeding the median. This will put a dampener on expectations for the coming season. However, I have a few thoughts when it comes to this projection: