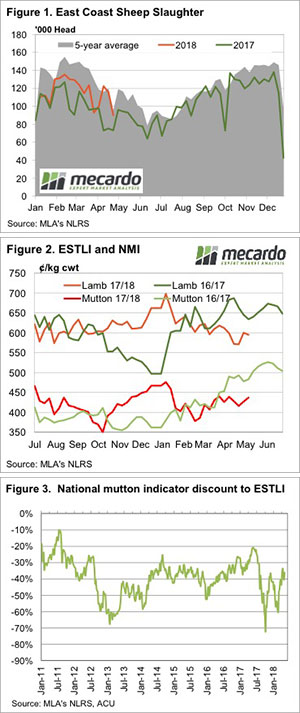

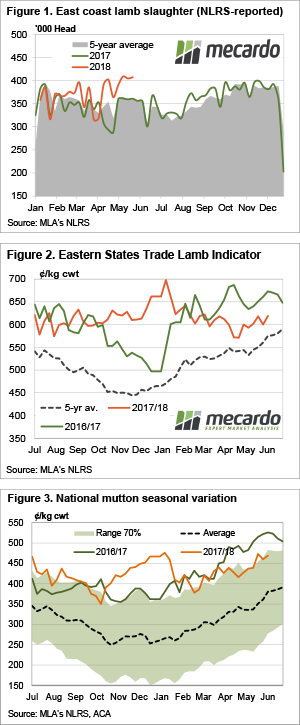

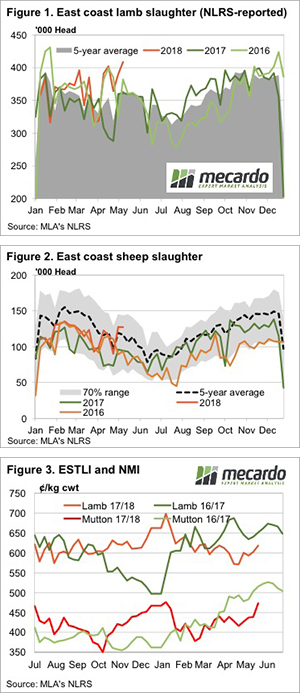

After the TFI fire in January, you’d have been thought crazy if you said that weekly east coast lamb slaughter would spend most of May above 400,000 head. Even crazier if you said sheep slaughter would be 30,000 head higher than last year, yet here we are.

After the TFI fire in January, you’d have been thought crazy if you said that weekly east coast lamb slaughter would spend most of May above 400,000 head. Even crazier if you said sheep slaughter would be 30,000 head higher than last year, yet here we are.

The confluence of strong lamb and mutton demand, and drought-induced strong supply has seen Victorian and NSW processors killing many more lambs and sheep than last year to keep up. East Coast lamb slaughter has never been above 400,000 head for three weeks in a row (Figure 1). It’s also been five years since this many sheep and lambs have been slaughtered in May.

Saleyard reports suggest the supply of finished lambs might be starting to wane, and this saw the Eastern States Trade Lamb Indicator (ESTLI) gain 18¢ to close at 619¢/kg cwt on Thursday, the highest price since March (Figure 2).

As we move into June, it is now that prices don’t look that great. Historically, anything over 600¢ is a good lamb price, but it’s becoming the norm in June. This will be the third year in a row, albeit prices are still around 10% behind the 2017 June price.

Mutton prices gained a little ground, with good mutton making over 500¢/kg cwt, and the average at 469¢. It wasn’t that long ago that $5 was a good price for lambs.

Over in the west, trade lambs were up 20¢ to 626¢/kg cwt, not quite matching Victoria at 630¢ but still very strong. WA mutton is lagging well behind however, at 390¢, but some good recent rain might help this.

The week ahead

Some of the 7 and 14-day rainfall maps are starting to show some precipitation for NSW. No guarantees, but if it eventuates we can expect a decline in sheep supply. This might coincide with annual plant maintenance shutdowns, but we still expect prices to strengthen over the coming month.

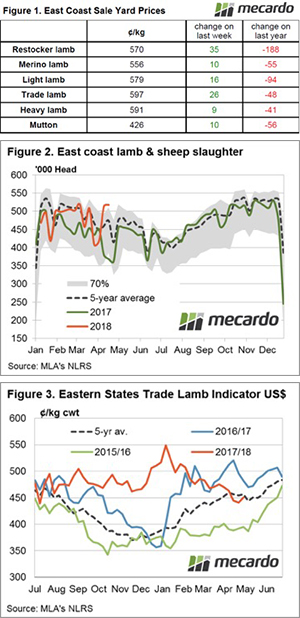

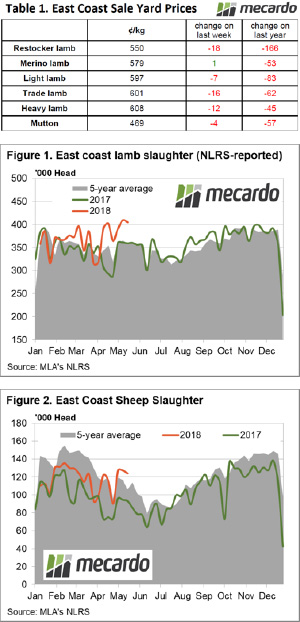

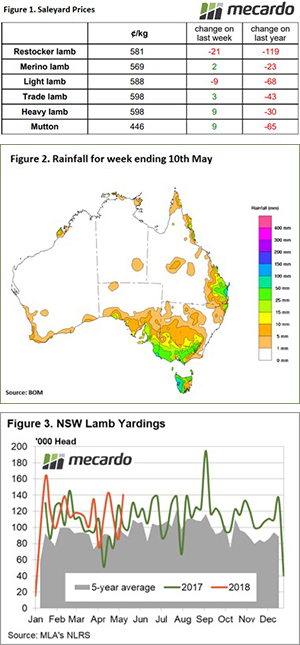

In the commentary last week, we noted that demand for lamb and sheep was keeping sale yard prices supported. Alas, it seems that supply has got the upper hand this week with East coast prices broadly softer. The Eastern States Trade Lamb Indicator (ESTLI) off 2.5% to 601¢/kg cwt and East Coast Mutton shaved off 1% to close at 469¢/kg cwt.

In the commentary last week, we noted that demand for lamb and sheep was keeping sale yard prices supported. Alas, it seems that supply has got the upper hand this week with East coast prices broadly softer. The Eastern States Trade Lamb Indicator (ESTLI) off 2.5% to 601¢/kg cwt and East Coast Mutton shaved off 1% to close at 469¢/kg cwt.

Winter officially arrives next week, and with it, we expect lamb slaughter to decline from recent record highs. Traditionally lamb supply throughout the winter is sustained by the last of the old season lambs, and the arrival of new season spring lambs out of NSW in the second half of July. With the dry continuing, we ask whether these lambs will finished on time, and whether they’ll be there at all.

Winter officially arrives next week, and with it, we expect lamb slaughter to decline from recent record highs. Traditionally lamb supply throughout the winter is sustained by the last of the old season lambs, and the arrival of new season spring lambs out of NSW in the second half of July. With the dry continuing, we ask whether these lambs will finished on time, and whether they’ll be there at all.

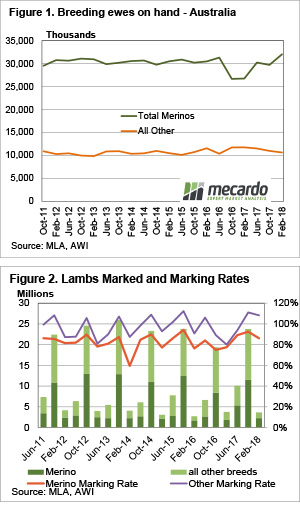

beginnings of the Autumn break, with some light falls extending into NSW – Figure 2. The arrival of the rains has certainly stemmed the decline of lamb and sheep prices in Victoria with sale yard NLRS reporting modest gains of up to 2% across nearly all categories. Victorian Restocker Lambs the exception, closing 4% softer to 573¢/kg cwt.

beginnings of the Autumn break, with some light falls extending into NSW – Figure 2. The arrival of the rains has certainly stemmed the decline of lamb and sheep prices in Victoria with sale yard NLRS reporting modest gains of up to 2% across nearly all categories. Victorian Restocker Lambs the exception, closing 4% softer to 573¢/kg cwt.