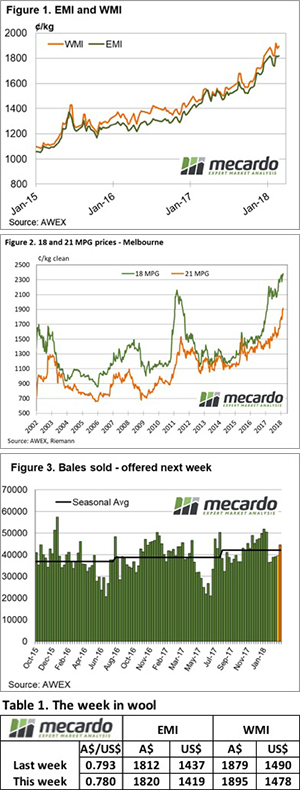

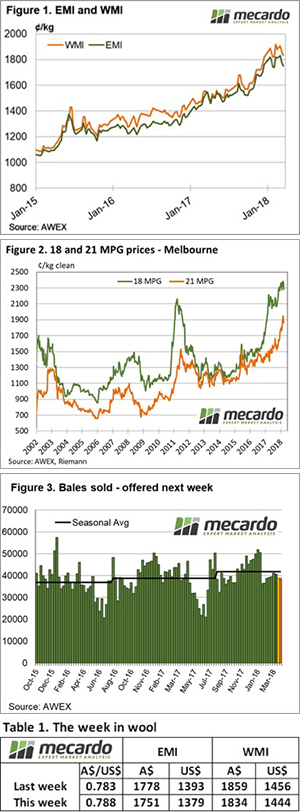

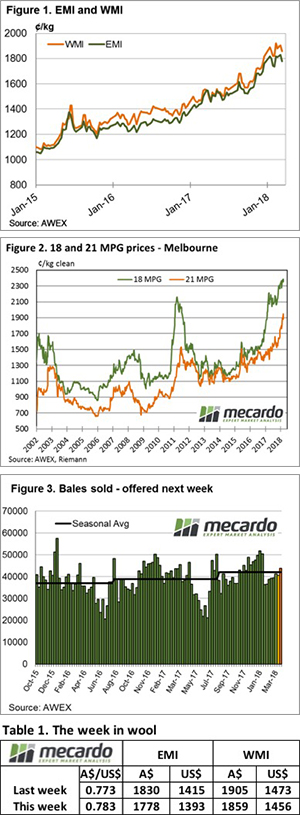

Another week with red splashed across the board for the wool market. The price retractions were not as severe as last week, yet the further correction meant buyers were more selective with their purchases resulting in significant discounts or rewards for quality.

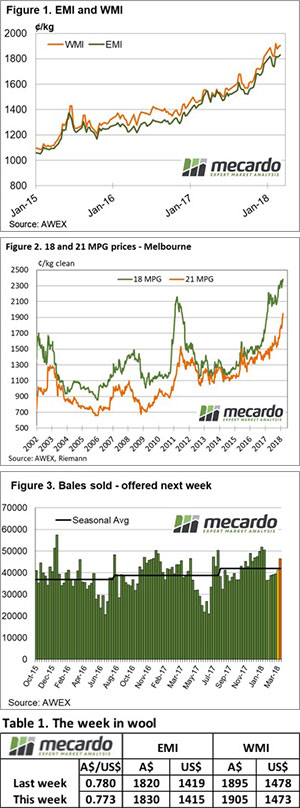

Even on opening, the market began its slide further into negative territory for most categories. By the close on Thursday, the Eastern Market Indicator (EMI) had fallen 27 cents to 1751 cents, while in US$ terms the drop was just 13 cents (Figure 1). The AU$ found additional strength during the week, edging up to $0.788, which was evident in the market indicators. The story was similar in the West. The Western Market Indicator (WMI) seeing a 25 cent reduction to 1834 cents.

A reduction in prices meant buyers were able to be more picky with their purchases. AWEX reported that small impurities, which were being overlooked in the rising market, didn’t make it past buyers eyes unnoticed this week and received significant discounts. In particular, wools with high mid breaks of greater than 75 struggled to make the cut. But this also meant that lots possessing mid breaks of less than 40 were rewarded with attractive premiums.

Fine fibres of 19 micron and less were generally subject to reductions of 60 to 70 cents In Northern and Western selling centres. Losses for broader microns averaged 30 to 45 cents. The Southern region was much more forgiving however. Wools of 18.5 to 22 micron seeing drops hovering around 10 cents.

Crossbred types reflected similar outcomes to the Merino market with prices generally discounted between 10 and 20 cents from last week. Merino skirtings saw some mixed results. Those with high VM were heavily discounted while some favoured lots with VM below 5% retained their ground.

As would be expected, the further fall in the market left growers unappeased, leading to a pass in rate of 9% for the 42,645 offered to the trade.

The week ahead

Next week there is 38,849 bales forecast on offer for the three selling centres. A 9% drop on this week’s offering. Two days of sale on Wednesday and Thursday are set for each Sydney, Melbourne and Fremantle.

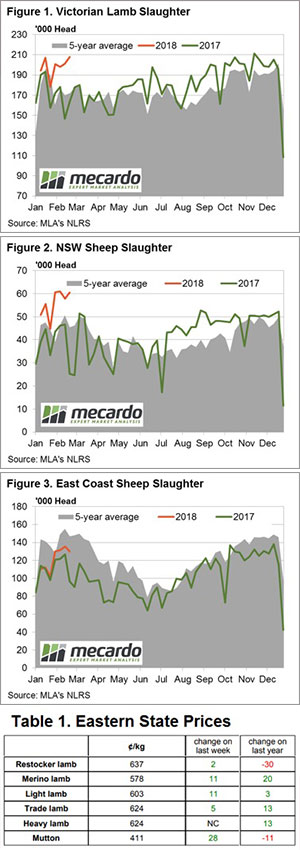

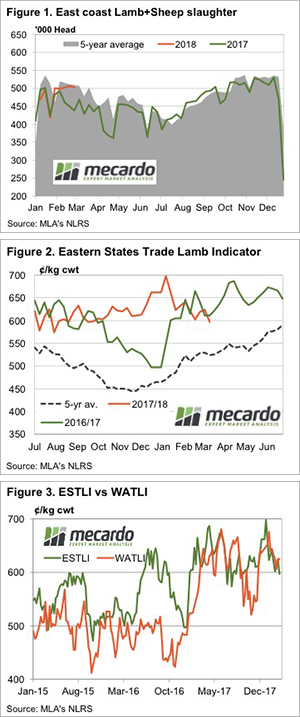

The broad trend in East coast lamb and sheep slaughter numbers continue to be dominated by NSW and Victorian flows at the moment with a spike in lamb slaughter in the previous week, to levels well above normal, unable to dampen prices too vigorously. Similarly, elevated throughput along the East coast for both lamb and sheep was powerless to inhibit demand, particularly for mutton and Merino lamb.

The broad trend in East coast lamb and sheep slaughter numbers continue to be dominated by NSW and Victorian flows at the moment with a spike in lamb slaughter in the previous week, to levels well above normal, unable to dampen prices too vigorously. Similarly, elevated throughput along the East coast for both lamb and sheep was powerless to inhibit demand, particularly for mutton and Merino lamb.

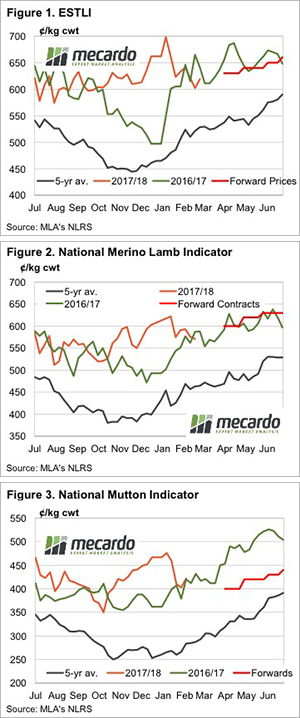

Earlier this week the first forward contract prices for lambs and mutton for the April to July period were released. While there were few surprises on the pricing front, it’s worth taking a look at the values, and how they compare to historical price movements, and where prices were last year.

Earlier this week the first forward contract prices for lambs and mutton for the April to July period were released. While there were few surprises on the pricing front, it’s worth taking a look at the values, and how they compare to historical price movements, and where prices were last year.