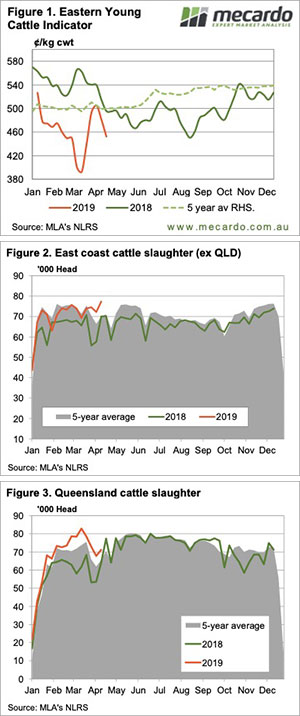

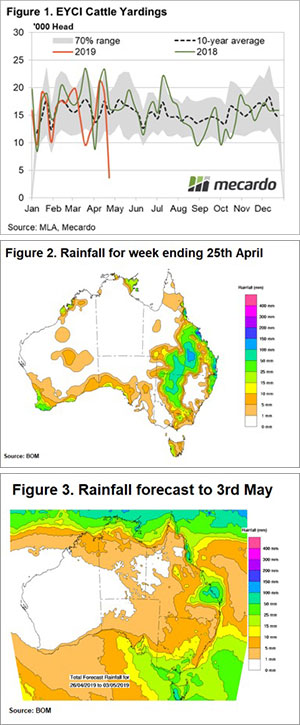

A combination of low saleyard volumes and rainfall have helped to shore up the Eastern Young Cattle Indicator (EYCI) this week amidst the Easter and ANZAC public holidays, which have provided limited cattle sale opportunities.

The shortened trading week due to the Easter break and ANZAC commemorations have seen EYCI eligible cattle yardings slump to the lowest weekly levels this season.

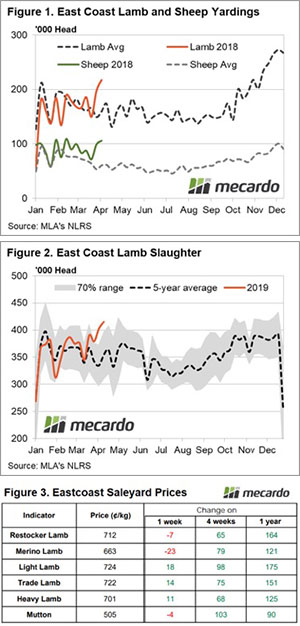

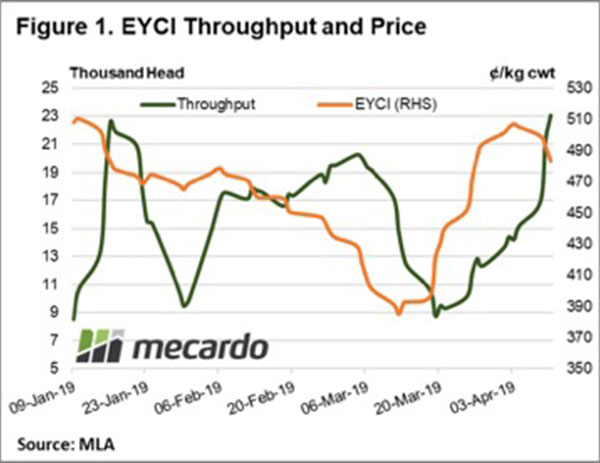

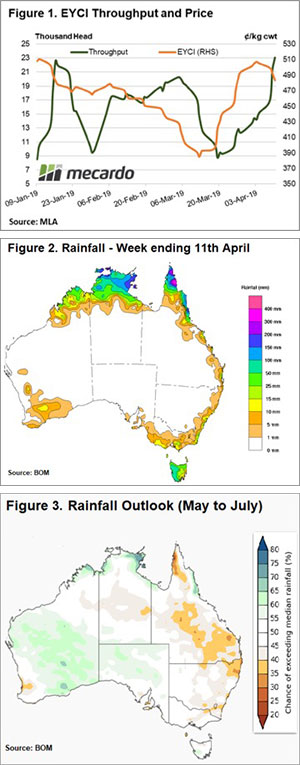

EYCI average weekly yardings have dipped to a mere 3,600 head this week, 59% below the levels seen during the Easter hiatus in 2018 and moved well below the normal range (as identified by the grey shaded zone in Figure 1). In contrast, the 2018 Easter dip toward 8,750 head, which occurred in early April, tested the lower end of the normal Easter throughput range.

The low volume of EYCI eligible cattle offered at sales this week has seen the EYCI bounce 3.6% to close at 468.75¢/kg cwt. Reasonable rainfall in southern Queensland and western NSW is boosting optimism (Figure 2).

However, it was a bit of a mixed bag for other cattle types. According to the Eastern States NLRS reported data, Medium Cow gained 9% to hit 205¢/kg lwt. In contrast, Heavy Steers eased 1.3% to close the week at 275.75¢/kg lwt.

In offshore markets the 90CL frozen cow indicator continues to push higher, reportedly cracking above 690¢/kg CIF prior to the Easter break. This is the highest the 90CL indicator has been in A$ terms since October 2015 when US demand for imported grinding beef was running red hot.

Next week

There is some follow-up rain scheduled for this week, particularly for south-east Queensland and Victoria. It is probably too early to call a start to the Autumn break in the south but it should be enough to keep cattle prices firm as we resume normal saleyard operations into next week.

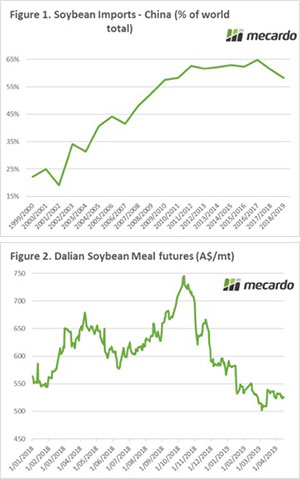

This buying by consumers is an attempt to ensure that they have some cover as we start the new season marketing period. There is still great uncertainty on how the season will transpire, however, the memory of the past year is fresh – and A$339 is more attractive than a possible >A$400.

This buying by consumers is an attempt to ensure that they have some cover as we start the new season marketing period. There is still great uncertainty on how the season will transpire, however, the memory of the past year is fresh – and A$339 is more attractive than a possible >A$400.