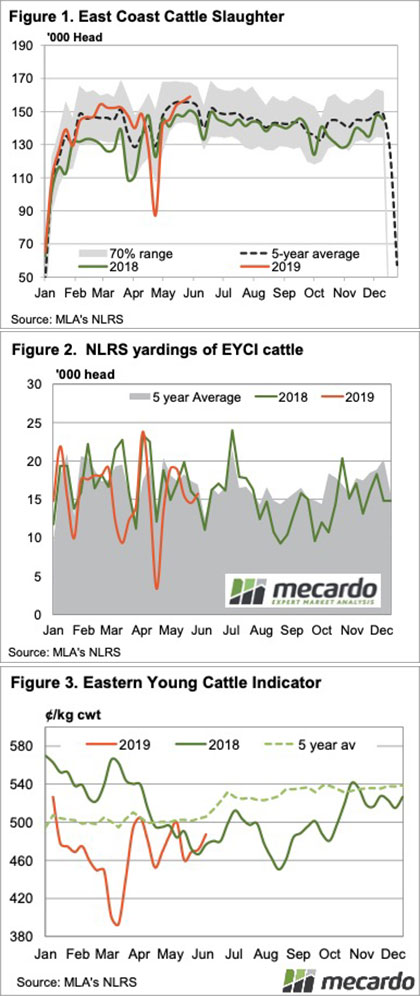

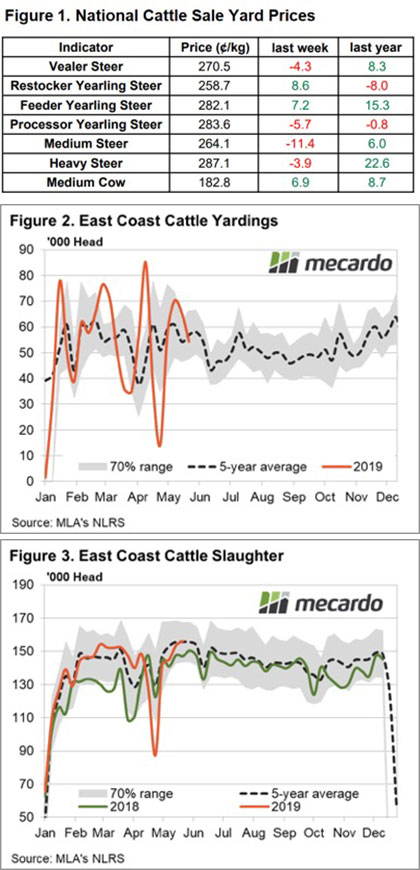

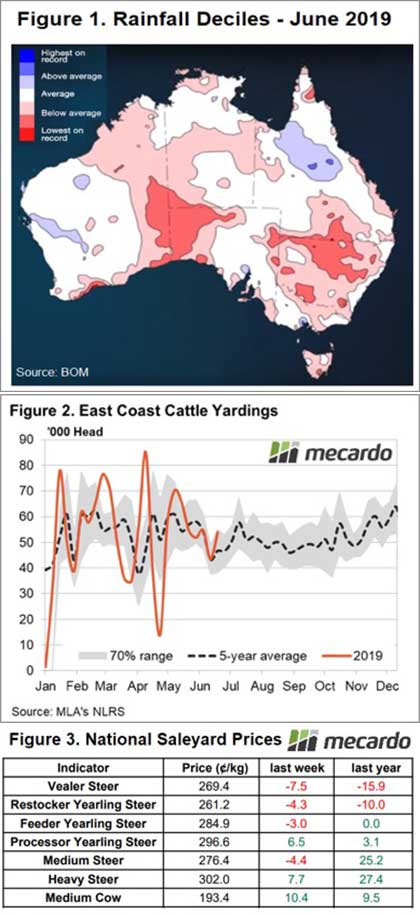

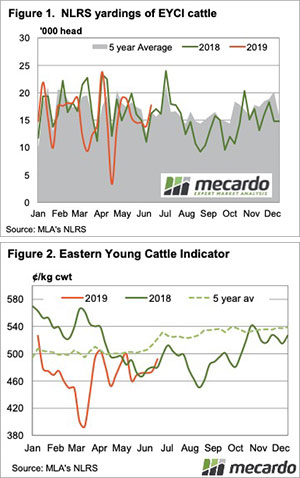

The Eastern Young Cattle Indicator (EYCI) managed to eke out a limited gain this week, lifting 4.45¢ to close at 520¢/kg cwt. Limited rainfall across much of the nation, except Victoria, acted as a headwind. Meanwhile, tightening supply across the east coast stopped the market from tanking too much.

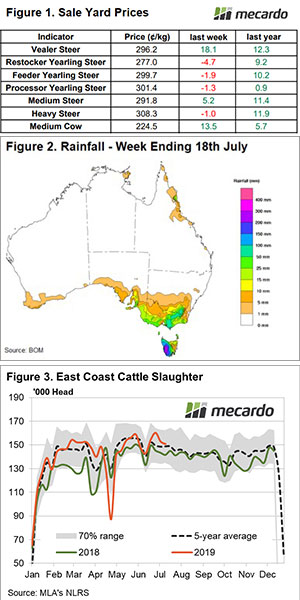

National sale yard cattle indicators for the week were somewhat mixed, albeit within a narrow range with the opposing forces of limited rain and reduced supply keeping markets in a broad sideways pattern.

Yearling and Heavy Steers were marginally softer, coming in 1¢-5¢ lower across the nation. Vealer and Medium Steers, along with Medium Cow managed a little better with gains between 5¢-18¢ noted – Figure 1*. The National Vealer Steer indicator was given a significant boost this week by a large jump in WA Vealer Steer prices, up nearly 92¢ to close at 309.2¢/kg lwt.

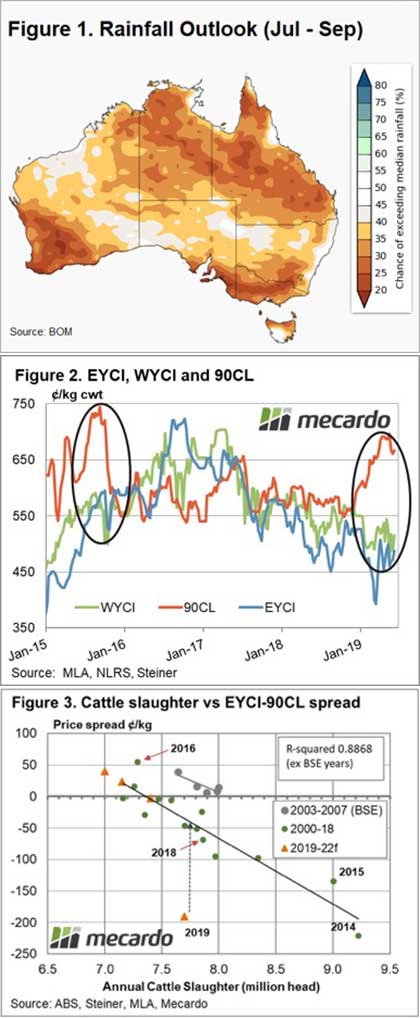

It probably comes as no surprise given the rainfall pattern this week (Figure 2) but cattle prices in Victorian sale yards showed the most vigour across the states with gains between 8¢-23¢ noted for all reported categories, except Victorian Vealer Steers.

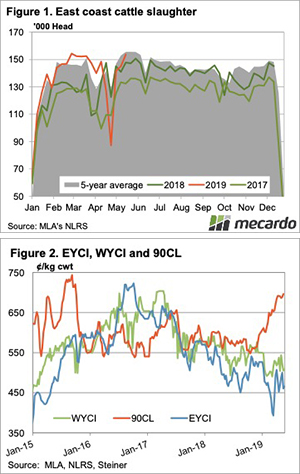

Looking at the east coast slaughter trend in recent week we have seen levels begin to trend lower since the start of July – Figure 3. A few weeks back we were processing around 160,000 head a week across the east coast, currently we are running at around 150,000 head and its likely in a few weeks’ time numbers will ease toward the 140,000 head region. That’s if the market follows along roughly with the average seasonal trend (black dotted line on Figure 3).

* All cattle prices in Figure 1 are expressed in ¢/kg lwt terms

Next week

The rainfall forecast for the coming week shows a repeat of this week, with falls limited to Victoria, coastal SA and the south west tip of WA. Limited rainfall on the horizon and the prospect of a dry finish to winter and a dry start to spring won’t do a lot to get cattle prices moving aggressively higher.

Seems like it’s a continuation of the sideways moves for the near term. If you are getting bored watching the sideways moves of the cattle market check out the 2004 comedy/drama Sideways over the weekend – its worth a laugh or two.

Restocker Steer prices between Victoria and NSW showing the impact of the recent Victoria rains with Victorian Restocker Steers commanding a 30¢ premium over NSW to record a 38¢ gain on the week to close at 258.4¢/kg lwt. Despite the rainfall in Victoria in recent weeks the longer-term outlook is worrying.

Restocker Steer prices between Victoria and NSW showing the impact of the recent Victoria rains with Victorian Restocker Steers commanding a 30¢ premium over NSW to record a 38¢ gain on the week to close at 258.4¢/kg lwt. Despite the rainfall in Victoria in recent weeks the longer-term outlook is worrying.