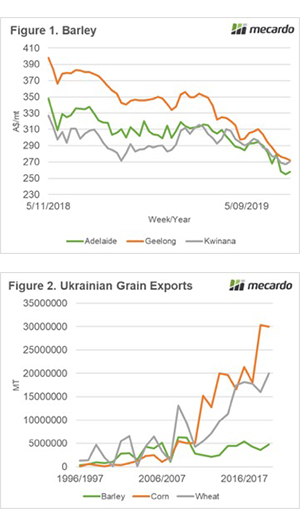

This year sees the opening of the T-Ports facility on the Eyre Peninsula. This facility brings additional export capacity and with that the potential for extra competition. In this update, we examine the historical spreads between Adelaide and Port Lincoln.

In recent days there has been commentary that the spread between Port Lincoln and Adelaide had narrowed as a result of the introduction of the T-Ports facility. We thought it was worthwhile to examine the historical spreads between the two-port zones.

The T-Ports facility is based at Lucky Bay and utilizes a different loading method from any other grain export port in Australia. Up until now, grain in Australia was loaded onto vessels in Australia direct from a berth, T-Ports will use a transshipment vessel.

The transshipment vessel ‘Lucky Eyre’ will load grain at Lucky Bay, which will then sail to deep water vessels to transfer the grain onboard. This is a relatively common way of loading vessels in regions where vessel drafts are an issue.

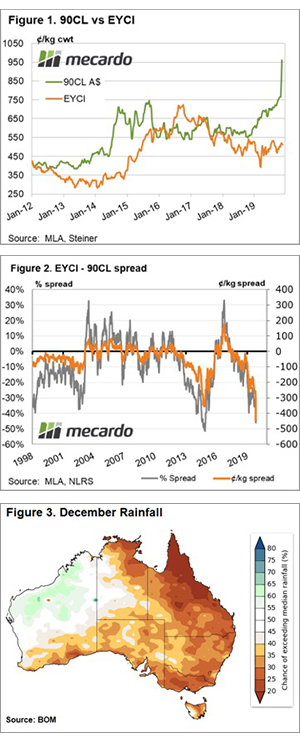

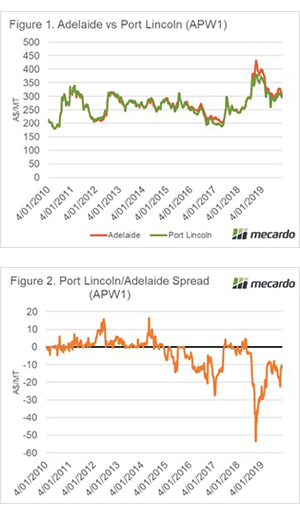

In figure 1, the historical prices for APW1 are shown for Adelaide and Port Lincoln. Typically, Adelaide and Port Lincoln have traded at similar levels for much of the past decade. There have, however, been periods when Adelaide has traded at a strong premium, especially during the past 18 months.

This spread is clearly displayed in figure 2. This chart represents the premium or discount between Port Lincoln and Adelaide. Last year saw the discount at its largest level versus the rest of the decade. However, recent months have seen the spread narrow.

There is some speculation that this narrowing of the spread is due to the extra competition encouraging buyers. However, at present, it is hard to confirm whether competition is the cause.

We do know, however, that last year Adelaide was pricing into the eastern state domestic homes, rather than the export market. As the market has come off the boil, Adelaide pricing has fallen dramatically. It is more than likely that the larger discount at Port Lincoln last year was a result of the cost of logistics to the domestic market.

What does it mean?

The T-Ports facility is a fantastic addition to the Australian grain export market. This model is one that can be rolled out in further regions, at a potentially lower cost than traditional berth-based discharging.

Grain growers on the Eyre Peninsula now have additional options for delivering their grain, which will in many areas reduce their freight costs.