Last Thursday while Melbourne & Fremantle continued to lift, Sydney didn’t sell, so this week the market between centres firstly had to realign. This saw Melbourne down and Sydney up on Wednesday, however when the dust had settled at the close of the week there was a feeling of relief that the market overall was positive following a couple of tumultuous weeks.

Despite much speculation before the market opened that this week would see much of last weeks gains returned, the result was strong with a steady demand from buyers at the current market levels.

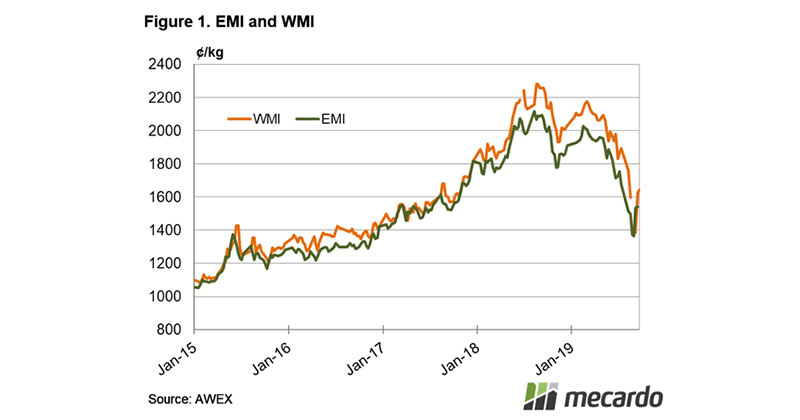

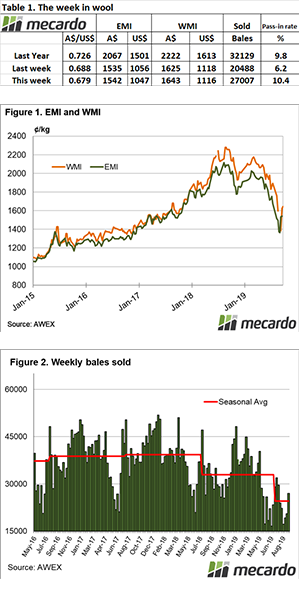

The Eastern Market Indicator (EMI) lifted 7 cents or 12% for the week, to finish at 1,542 cents. The Aus$ fell slightly to US $0.679. This saw the EMI in US$ fall by 9 cents to end the week at 1,047 cents.

Western Australia again had a positive result. The Western Market Indicator rose by 18 cents to close at 1,643 cents .

Again, it was the finer types that performed strongest, reflected across the three selling centres. Crossbreds were generally unchanged, however the Merino Cardings Indicators in Sydney and Fremantle lifted, with the 1,000-cent mark again in sight.

30,135 bales were offered to sale with 10.4% passed in. This saw 27,007 bales cleared to the trade (Figure 2). There have been 102,227 fewer bales sold this season compared to the same period last year. This is an average weekly gap of 11,359 bales.

The dollar value for the week was $47.09 million, for a combined value so far this season of $377.78 million.

The week ahead

Next week just under 30,000 bales are rostered, with the roster only increasing marginally in subsequent weeks.

Although the volatile market is still playing on all participants minds, there is somewhat a feeling of restored confidence. With the much reduced supply compared to previous years, the market should at least hold these levels, although the recent big swings will no doubt cause the market to remain on edge.