The wool market tracked lower for Merino types this past week however crossbreds bucked the trend and continued to rally.

As for exports, Chris Wilcox, NCWSBA, reports that export volume is down 12% for the season to March, however as a reflection of the strong market export value is up by 3%.

Chinese activity was even more effected, with season to date exports down 17% and export value down by 1%. This could be viewed as a concern; our major customer taking less wool, or it could be viewed as a positive; other markets stepping in to spread the demand.

The Eastern Market Indicator (EMI) eased by 8 cents on the week to close at 1,952 cents. The US$ fell by almost 0.5 cents to US $0.697 and as a result, the EMI in US$ terms fell by 15 cents to end the week at 1,361 US cents (Table 1).

The Western Market Indicator (WMI) after gaining 28 cents last week, gave up 31 cents to 2,062 cents this week.

It was a much reduced offering of 32,801 bales that came forward this week. Growers passed in 12.9% of the offering. The break up was 9% in Sydney, 12.9% in Melbourne while Fremantle sellers passed in 18.1% of bales offered.

This meant 28,576 bales were cleared to the trade, almost 12,000 fewewr than last week. In the auction weeks since the winter recess, 1,263,967 bales have been cleared to the trade, 230,624 fewer than the same period last year. The average shortfall cleared to the trade compared to the same time last year now sits at 6,406 bales per week fewer.

The dollar value for the week was $58.3 million ($82.9 million last week) for a combined value of $2.907 billion so far this season. A simple calculation of $ value divided by bales sold gives us $2,039 per bale across all types for the week.

The only positive moves were for the Crossbreds, gaining another 10/15 cents but mainly confined to the 28 micron and finer. While Cardings in Melbourne & Sydney were largely unchanged, however Fremantle fell 25 cents.

The week ahead

The roster for the next few weeks is beginning to show the threatened decline in supply. Next week just 33,361 bales are rostered for sale with all centres selling on Wednesday and Thursday. The following weeks 30,719 & 33,360 bales are currently forecast.

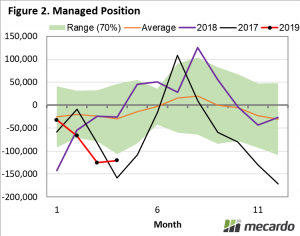

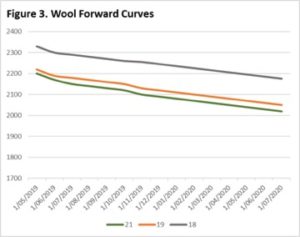

A solid week in the amount of forwards trades this week, especially for crossbreds which were collateral damage in this weeks’ auction market falls. Bets are on to see if prices continue to drop or level out again so it’ll be interesting to see developments in the coming weeks.

A solid week in the amount of forwards trades this week, especially for crossbreds which were collateral damage in this weeks’ auction market falls. Bets are on to see if prices continue to drop or level out again so it’ll be interesting to see developments in the coming weeks.

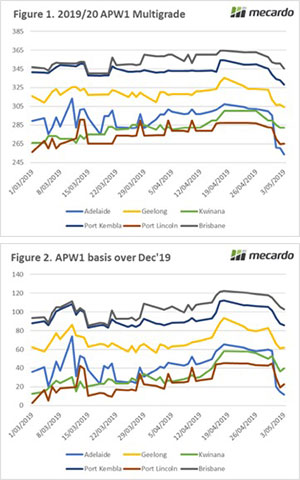

Figure 1 displays the physical contract price for APW1 multigrade and Figure 2 shows the basis versus December Chicago futures. I have selected a number of ports to give a broad spread of the nations’ wheat growing area.

Figure 1 displays the physical contract price for APW1 multigrade and Figure 2 shows the basis versus December Chicago futures. I have selected a number of ports to give a broad spread of the nations’ wheat growing area.

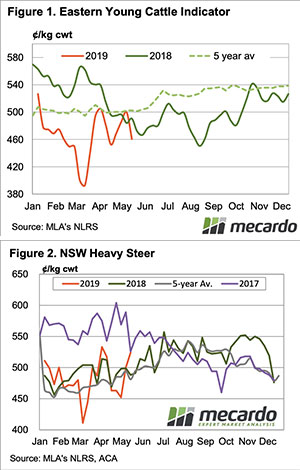

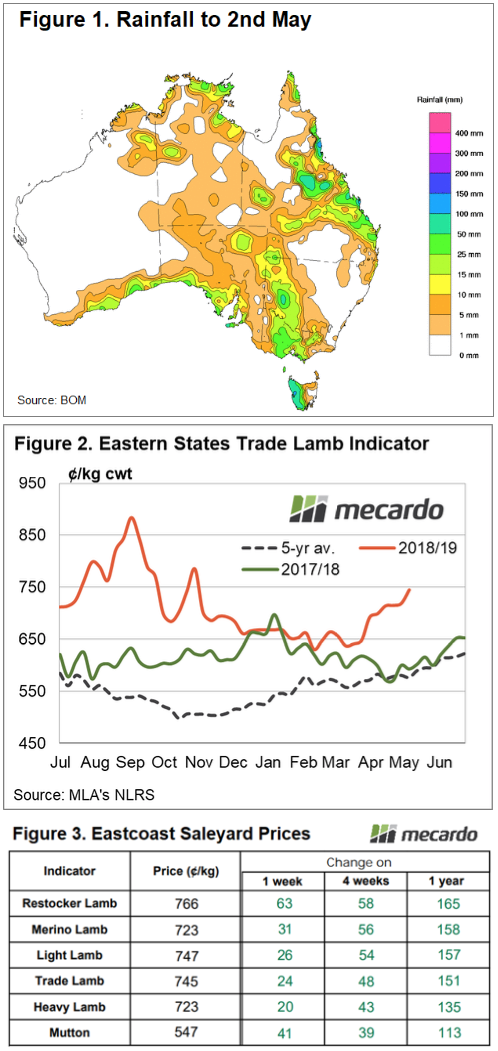

The Eastern States Trade Lamb Indicator (ESTLI) responding as expected to the improved climatic conditions with a 24¢ rally on pre ANZAC day prices from last week to close at 745¢/kg cwt yesterday. Expectations of tight lamb supplies as we head into winter has seen the ESTLI push higher earlier than last season and now sits over 150¢ higher than at this time during 2018 – Figure 2.

The Eastern States Trade Lamb Indicator (ESTLI) responding as expected to the improved climatic conditions with a 24¢ rally on pre ANZAC day prices from last week to close at 745¢/kg cwt yesterday. Expectations of tight lamb supplies as we head into winter has seen the ESTLI push higher earlier than last season and now sits over 150¢ higher than at this time during 2018 – Figure 2.

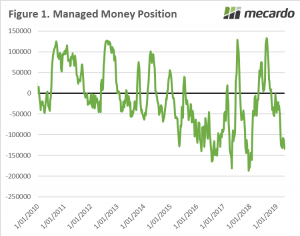

using a futures contract, it is either a long (buy) or short (sell) position.

using a futures contract, it is either a long (buy) or short (sell) position.