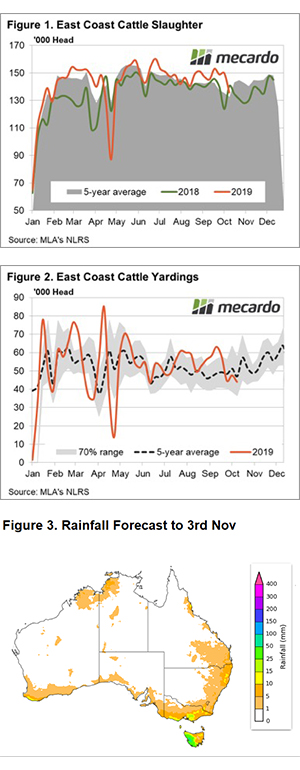

Significant increases to yarding levels for both lamb and sheep across the eastern states in recent weeks has started to weigh on prices. Higher than average lamb yarding was noted in Victoria but the big lift in lamb throughput was reserved for NSW. Mutton yarding levels were elevated in all east coast states.

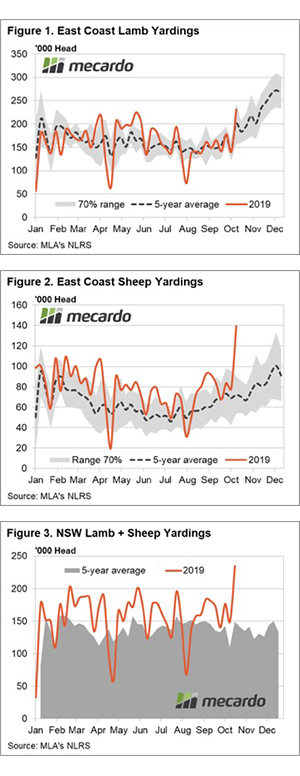

Weekly east coast lamb yardings levels hit a seasonal high last week at 231,591 head representing a 64% jump on the week prior. This places lamb yarding levels 16% above the five-year seasonal trend for this time in the year (Figure 1).

Lamb throughput in Victoria is trekking 9% ahead of the seasonal average but underpinning the jump in east coast lamb volumes at the saleyard has been NSW flows. Lamb yarding for NSW last week was up 48% on the week prior and is sitting 31% higher than the five-year average trend at 142,305 head.

Increased throughput wasn’t reserved for lambs alone with mutton numbers swelling too. Weekly east coast sheep volumes at the saleyard up 79% on the previous week to hit a seasonal high at 139,169 head. At this level east coast sheep yardings are sitting at massive 94% above the five-year seasonal average and you would have to go back to 2006 to find a higher weekly east coast sheep throughput level (Figure 2).

Higher than average sheep yardings were noted across all east coast mainland states with SA 42% above the five-year level, Victoria 51% higher and NSW, again underpinning the broader east coast figures, with sheep yarding levels 135% higher than the seasonal trend for this time in the year. Figure 3 shows the combined lamb and sheep throughput for NSW and it demonstrates how unusual this increase in saleyard volume is.

The National Trade Lamb Indicator (NTLI) feeling the brunt of the increased supply easing 4.2% this week to close at 770¢/kg cwt yesterday. Unsurprisingly, NSW Trade Lambs were lower too, slumping 4.8% to finish at 783¢/kg cwt. The National Mutton Indicator (NMI) eased 2.1% this week to 555¢/kg cwt. NSW mutton prices holding up well considering the elevated supply in recent times, dipping just 2.2% to close at 577¢/kg cwt.

Next week

The Victorian spring flush is underway but the significant numbers we see into November are yet to come. There is some rain forecast for Victoria this week which will allow producers to hold lambs for a bit longer if they are keen. Prices favour a downside bias until some of the Victorian supply is able to be accounted for.