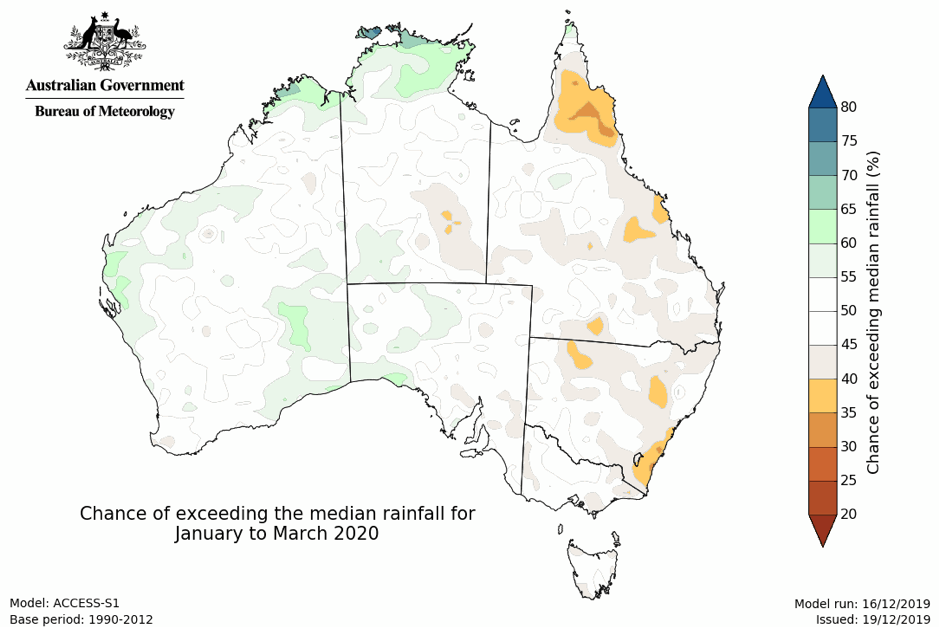

A welcome sound not heard for a long time is being heard throughout large parts of NSW & QLD. The noise of raindrops hitting roofs. This week we cover a few factors from overseas impacting on markets including Egyptian purchases, Russian intervention, and the phase 1 deal.

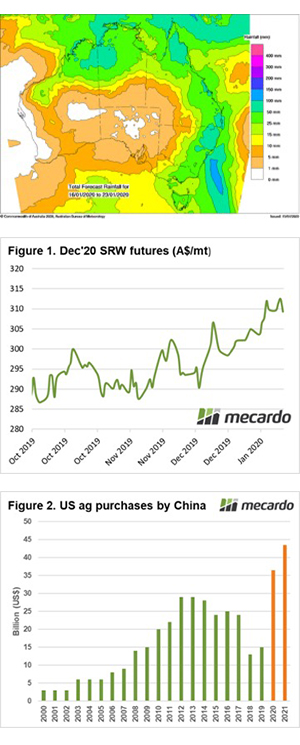

In recent months weather forecasts have consistently tantalized without providing much (see map). Last week strong rainfall was forecast for large parts of the country, and like the boy who cried wolf – I didn’t believe the forecasts. As time flowed this one seemed to be coming to fruition, but I had been tricked into a false sense of security before.

To my delight, this one has delivered for many. Although this rainfall event would have been more welcome four weeks ago for the summer crop, it has provided a good dump of rain throughout the drought-ridden east coast. Let’s not get too cocky though, we’ll need a little more rain to guarantee a good 2020 crop.

Let’s start with the global market. At the end of last week, the Chicago futures market rallied as Egypt bought 300kmt of wheat, at the highest price since February. This volume was unsurprisingly black sea origin however provided a bullish sentiment for overall pricing.

Russia also assisted with the price rise by intervening in their markets. A new export quota limiting grain exports to 20mmt for the first half of the year was enacted. This caused some concern as interventions by what is now the world’s most important grain exporter could have ramifications for trade flows.

Relations between China and the US seemed to be thawing this week, as both countries agreed to a phase 1 trade deal. This deal is a starting point in improving trade between the two super powers, including the agreement to purchase an increased value in agricultural produce over the next two years.

In the agreement China are set to purchase $36.5bn (A$52bn) in 2020, and $43.5bn(A$63bn) in 2021. To put the scale of the increase in perspective during 2017 China purchased $24bn (A$35bn) in agricultural produce from the US (figure 2).

There is a lot of conjecture at present related to which commodities China will purchase in order to increase their value purchased.

The trade wasn’t overly impressed by the deal as it didn’t contain much detail in regards to products purchased, and included a market value clause:

‘The Parties acknowledge that purchases will be made at market prices based on commercial considerations and that market conditions, particularly in the case of agricultural goods, may dictate the timing of purchases within any given year.’

The big concern for me is that in order to meet these purchase requirements is that the trade flows may prioritise US as an origin for many agricultural commodities.

Remember to listen to the Commodity Conversation podcast by Mecardo

What does it mean/next week?:

The rain is set to continue through many parts which will provide some confidence for the coming crop. This must be tempered by the reality of it being four months until seeding and nine months from harvest.

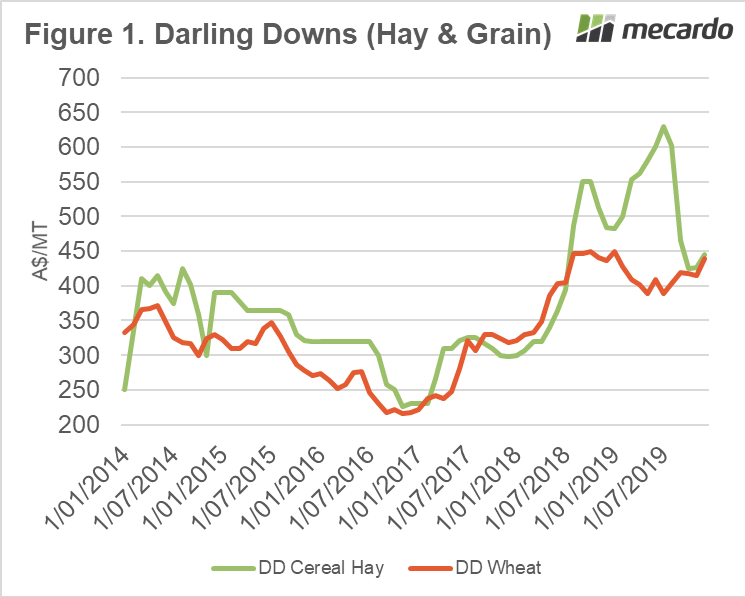

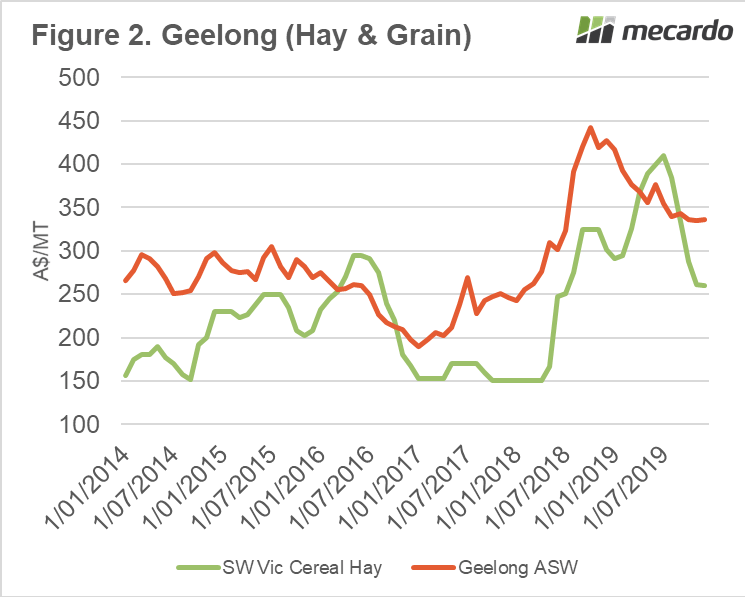

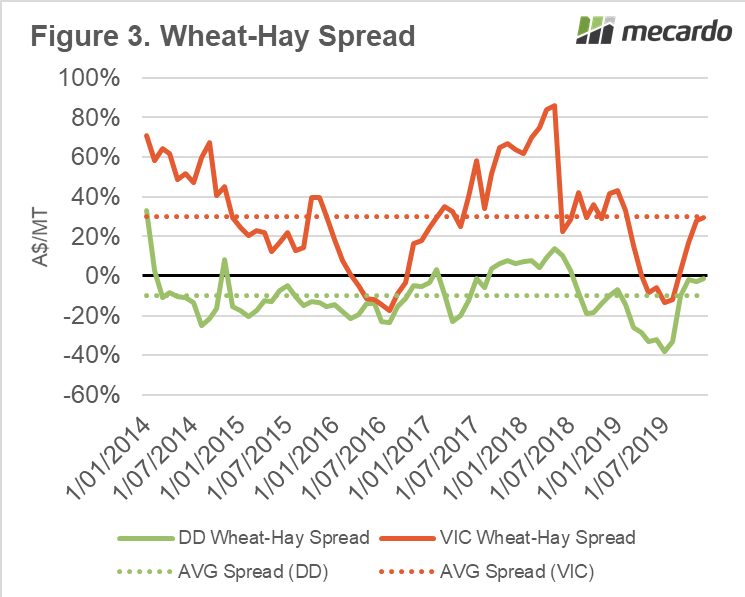

Our team covers a range of commodities, from goats to fertilizer. One of the agri products which we have not covered in much detail has been fodder due to the lack of available data. However we will now start to include the fodder market on a regular basis.

Our team covers a range of commodities, from goats to fertilizer. One of the agri products which we have not covered in much detail has been fodder due to the lack of available data. However we will now start to include the fodder market on a regular basis. The focus is on the Darling Downs and Victoria. This is since the Darling Downs is the primary demand driver and Victoria is likely to be the supplier this season.

The focus is on the Darling Downs and Victoria. This is since the Darling Downs is the primary demand driver and Victoria is likely to be the supplier this season. This spread is shown as a percentage since 2014 in figure 3. On average wheat is at 10% discount on the Darling Downs, whereas Victoria holds a 30% premium.

This spread is shown as a percentage since 2014 in figure 3. On average wheat is at 10% discount on the Darling Downs, whereas Victoria holds a 30% premium.

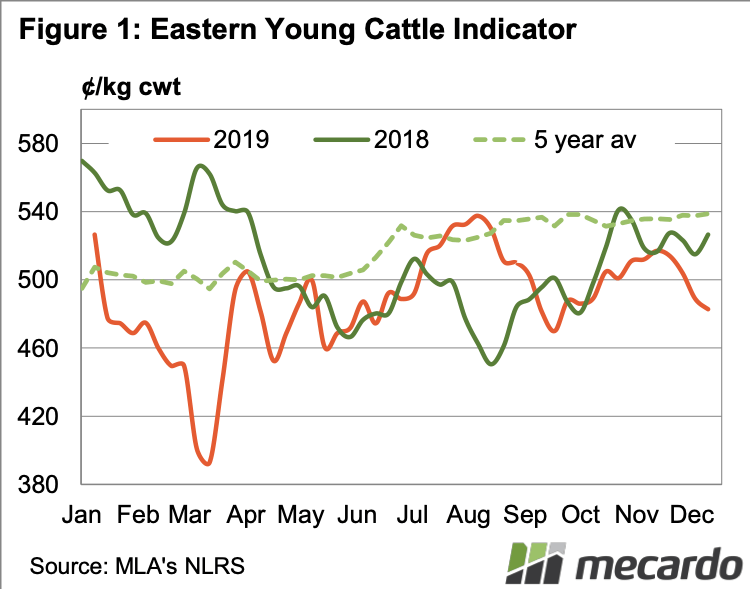

The Eastern Young Cattle Indicator (EYCI) has finished the year at a three month low, but it was on the back of yardings of just over 8,000 head. Figure 1 shows the final price for 2019 of 482.75¢/kg cwt is now 44¢ behind where it ended 2018.

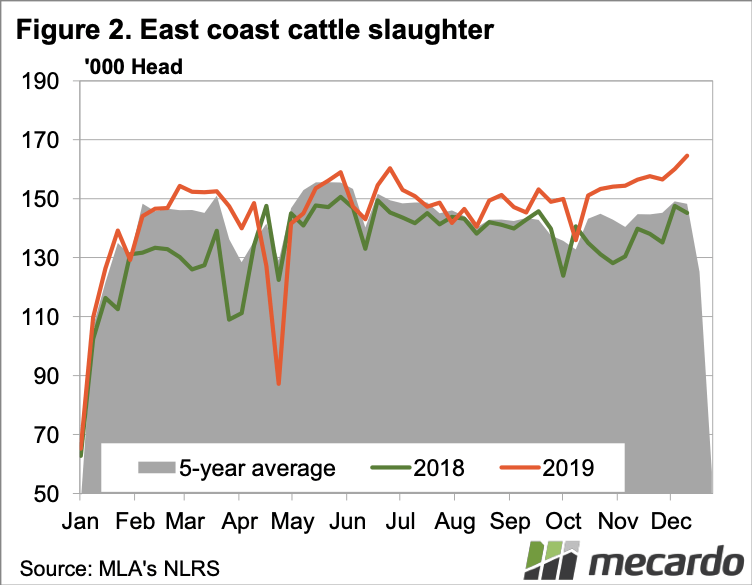

The Eastern Young Cattle Indicator (EYCI) has finished the year at a three month low, but it was on the back of yardings of just over 8,000 head. Figure 1 shows the final price for 2019 of 482.75¢/kg cwt is now 44¢ behind where it ended 2018. it is unusual for it to be the high for the year (figure 2).

it is unusual for it to be the high for the year (figure 2).

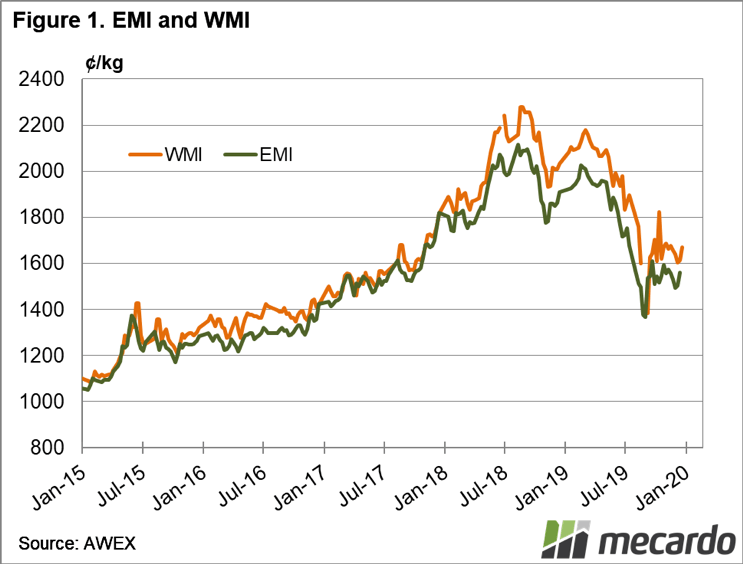

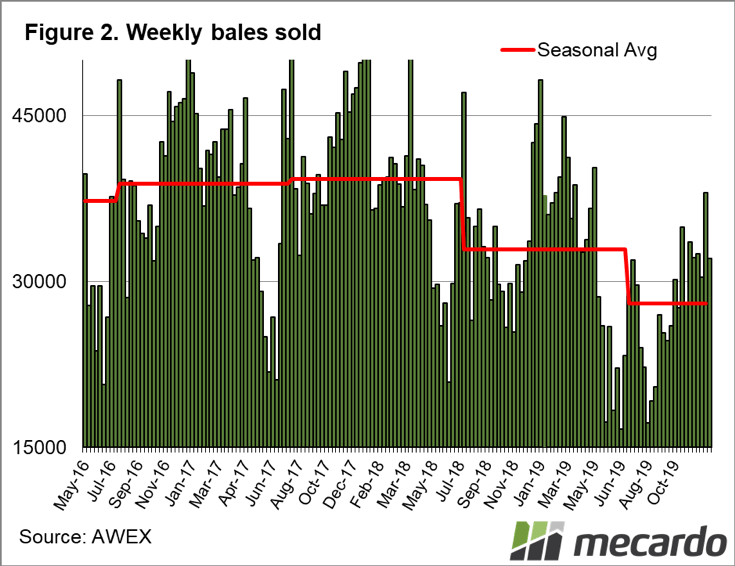

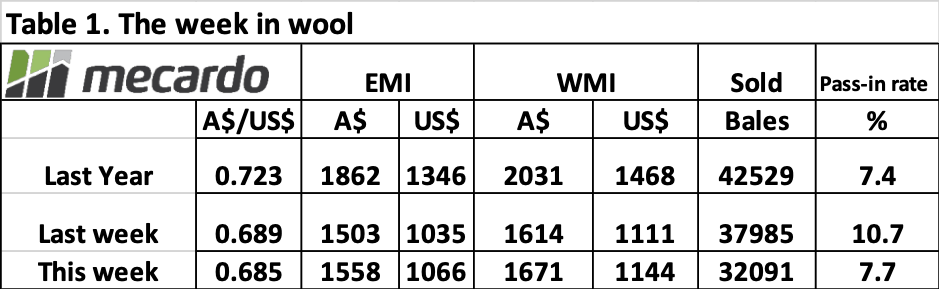

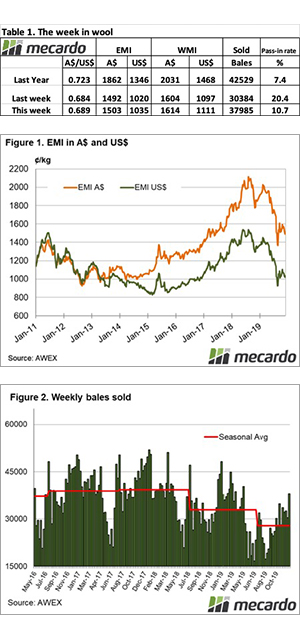

The Eastern Market Indicator (EMI) lifted 55 cents for the week to close at 1,558 cents. The AU$ gave up .05 cents to sit at US $0.645. In US terms, this pushed the EMI up 32 cents to 1,066 cents.

The Eastern Market Indicator (EMI) lifted 55 cents for the week to close at 1,558 cents. The AU$ gave up .05 cents to sit at US $0.645. In US terms, this pushed the EMI up 32 cents to 1,066 cents. Bales sold were 5,895 bales fewer than last week, and 10,438 down on the last week in 2018. The total lag in bale clearance from this season to last is currently at a difference of 119,995 bales.

Bales sold were 5,895 bales fewer than last week, and 10,438 down on the last week in 2018. The total lag in bale clearance from this season to last is currently at a difference of 119,995 bales.

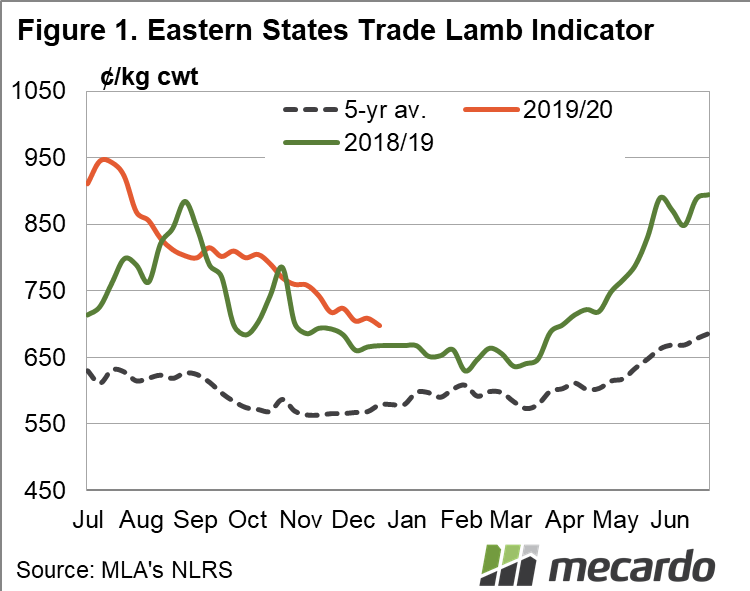

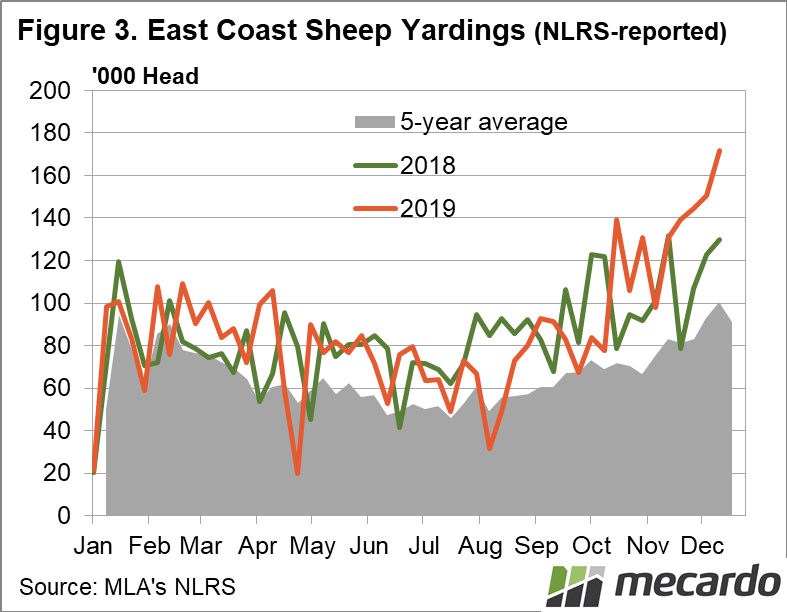

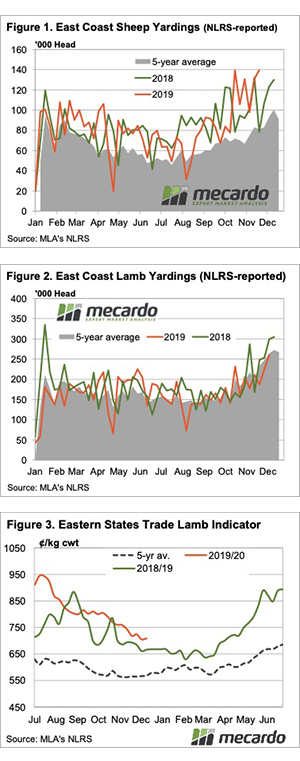

For the first time in 9 months the Eastern States Trade Lamb Indicator (ESTLI) dropped below the 700¢ threshold to end the week at 698¢. A hard number to swallow considering we’ve seen the ESTLI drop off nearly 250¢ from the record highs in July. That being said, this time last year the ESTLI was sitting at 668¢, so while the decline has been fast and hard, prices are still 4.5% higher than 2018.

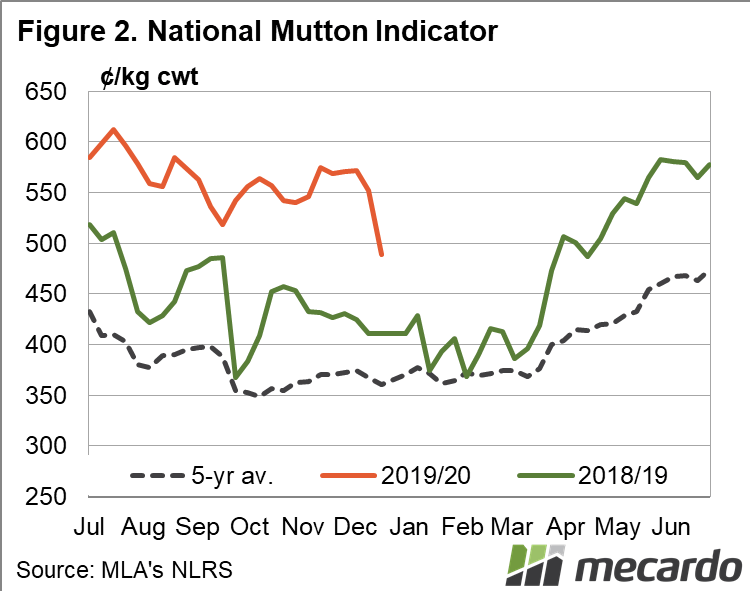

For the first time in 9 months the Eastern States Trade Lamb Indicator (ESTLI) dropped below the 700¢ threshold to end the week at 698¢. A hard number to swallow considering we’ve seen the ESTLI drop off nearly 250¢ from the record highs in July. That being said, this time last year the ESTLI was sitting at 668¢, so while the decline has been fast and hard, prices are still 4.5% higher than 2018. Mutton prices couldn’t hold on to finish the year at unbelievable levels. The National Mutton Indicator lost 79¢ on the week to close at 489¢. Another week of heavy mutton supply and the likely poor quality in NSW were the main drivers. All states contributed to the fall but NSW really took a dive. NSW mutton declined 13% on the week to 471¢/kg cwt.

Mutton prices couldn’t hold on to finish the year at unbelievable levels. The National Mutton Indicator lost 79¢ on the week to close at 489¢. Another week of heavy mutton supply and the likely poor quality in NSW were the main drivers. All states contributed to the fall but NSW really took a dive. NSW mutton declined 13% on the week to 471¢/kg cwt. Next Week.

Next Week.

The South Australian government is debating a bill to end the moratorium on GM crop cultivation. I received information from a contact related to claims from anti-gm activists. I thought it was time to dispel some of the activist’s misunderstandings.

The South Australian government is debating a bill to end the moratorium on GM crop cultivation. I received information from a contact related to claims from anti-gm activists. I thought it was time to dispel some of the activist’s misunderstandings.

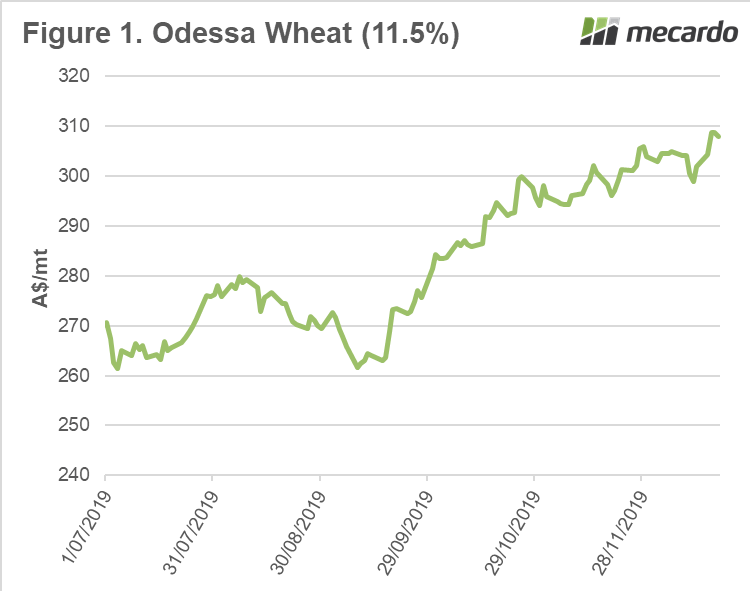

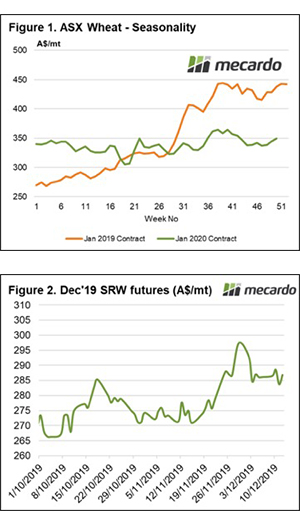

The ASX contract has risen dramatically during the past week, at the end of last week the December 2020 was trading at a weekly average of A$344 and has now moved up to A$349 (figure 1). There are concerns from feed consumers related to the slow pace of harvest in Victoria, which is driven both physical and futures levels higher.

The ASX contract has risen dramatically during the past week, at the end of last week the December 2020 was trading at a weekly average of A$344 and has now moved up to A$349 (figure 1). There are concerns from feed consumers related to the slow pace of harvest in Victoria, which is driven both physical and futures levels higher.