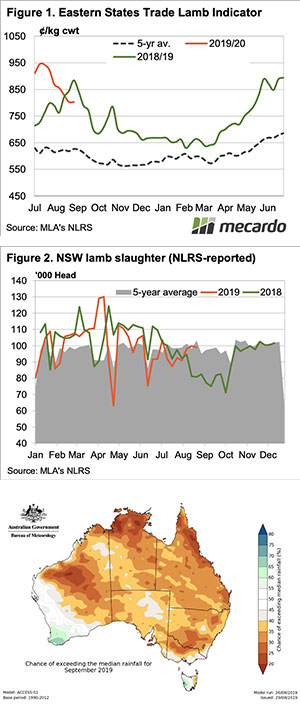

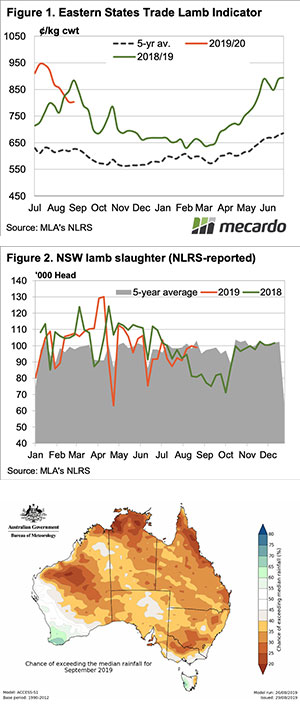

The Eastern States Trade Lamb Indicator (ESTLI) continues to hold above the 800¢ level as the Victorian flush shows no sign of getting underway yet. However, a jump in sheep yardings in recent weeks has seen the National Mutton Indicator (NMI) take a bit of a slide.

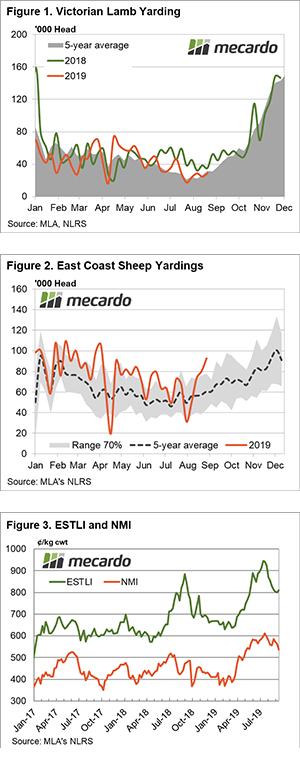

Victorian weekly lamb yarding numbers are running close to the five-year trend currently, just shy of 30,000 head, Figure 1. Last season a drier winter and spring saw numbers present earlier but this year the season has been relatively good for Victorian producers so there will be the opportunity to hold onto lambs to get the most out of their pasture.

The ESTLI seasonal spring decline has stalled in recent weeks as the east coast weekly lamb yarding numbers hover around the 150,000 head region. It is the surge in Victorian lambs we see during September to November that is usually the catalyst for the ESTLI to reach its seasonal low so the next leg lower in price isn’t likely to come until the Victorian throughput starts to swell.

Turning to markets with elevated throughput, East coast sheep yarding levels have been surging of late to see recent figures extend beyond the upper boundary of the normal seasonal range – Figure 2. Above average yarding levels in NSW a key driver of the high east coast figures with weekly sheep throughput over the last month averaging 36% above the five-year trend in this state.

NSW mutton prices reacting accordingly this week posting a 6.4% drop to close at 542¢/kg cwt and dragging the NMI lower too. The NMI finishing the week 4.8% softer at 536¢/kg cwt. In contrast, the ESTLI managed a slight gain, up 1% to rest at 811¢/kg cwt – Figure 3.

Next week

All eyes on Victorian lamb throughput levels in the next few weeks as that will be the clue to the timing of the next dip lower in the ESTLI. Our projections put the ESTLI trough this spring at around the 730¢/kg level in early November.

For the superstitious among us don’t do anything risky today – its Friday the 13th after all… and stay clear of black cats, just for good measure.

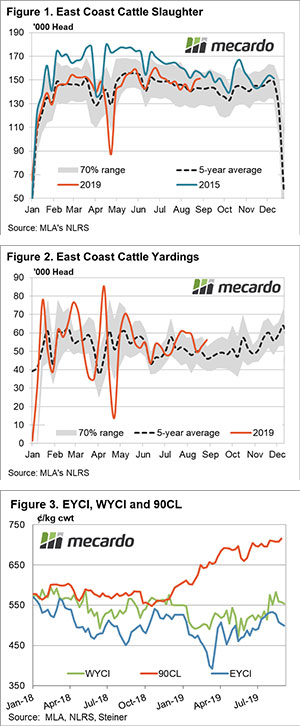

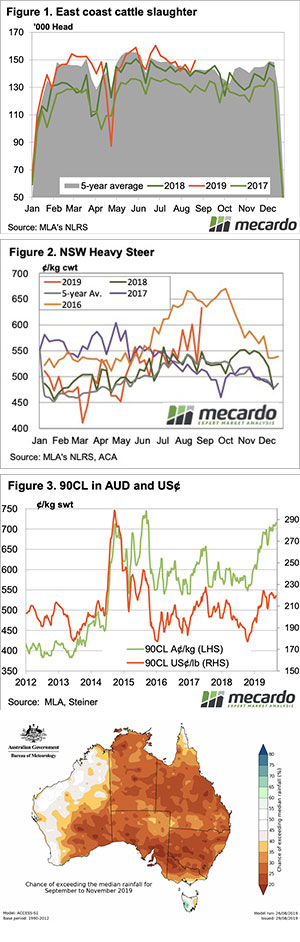

Despite rising slaughter rates, and more dry weather, the Eastern Young Cattle Indicator (EYCI) managed to find some support at 500¢. The demand from export markets remains rampant, with slaughter cattle prices hitting new peaks.

Despite rising slaughter rates, and more dry weather, the Eastern Young Cattle Indicator (EYCI) managed to find some support at 500¢. The demand from export markets remains rampant, with slaughter cattle prices hitting new peaks.